The Take Five Report: 8/31/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: +0.37%

- Dow: +0.10%

- Nasdaq: +0.48%

- Russell 2k: +0.40%

U.S. markets would advance moderately in yesterday’s session following the ADP Employment and GDP second estimate releases. Major indexes would open in the green, but be hit with a selloff in the first few minutes. The S&P and Nasdaq would go on to rally through the close, but the Dow would remain flatlined the rest of the way.

Asia:

- Shanghai: -0.55%

- Hong Kong: -0.55%

- Japan: +0.88%

- India: -0.39%

Asian markets closed mostly lower in this morning’s session. Chinese factory activity fell for the fifth straight month. In India, stocks were lower amid fresh allegations of trade manipulation of Adani Enterprises. Japan saw its retail sales rise to 6.4%, compared to the 5.4% expected.

Europe:

- UK: +0.12%

- Germany: -0.24%

- France: -0.12%

- Italy: +0.09%

European markets would pull back in Tuesday’s session and snap its multi day winning streak. Germany’s imports saw a decline in imports by -13.2%, the largest drop since January of 1987. Spain saw year over year inflation rise to 2.6%, which was in line with analysts' expectations.

I-II

U.S. Sectors Snapshot:

- Communication Services: +0.36%

- Consumer Discretionary: +0.33%

- Consumer Staples: +0.18%

- Energy: +0.51%

- Financials: +0.12%

- Health Care: -0.03%

- Industrials: +0.44%

- Info Tech: +0.83%

- Materials: +0.15%

- Real Estate: +0.35%

- Utilities: -0.43%

II

Technicals:

II-I

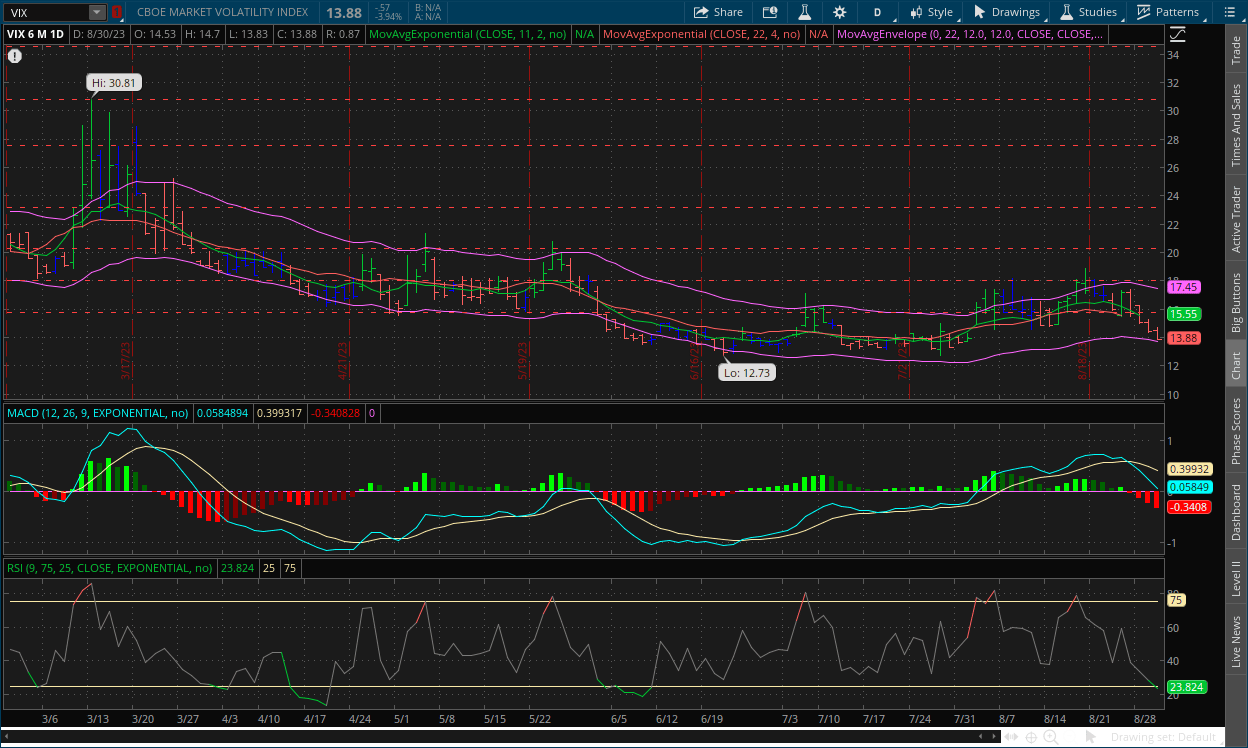

Volatility Index: (VIX)

Wednesday Recap:

The VIX would open the session slightly higher than Tuesday’s close at $14.58, and reach a high of $14.70 fairly early on. Prices would slide for most of the day, reaching a low of $13.83 before closing at $13.88.

Daily Chart:

Strength would move in favor of the VIX bears for the fourth straight session as they continue to overwhelm the VIX bulls. Inertia would continue to move in favor of the VIX bears as well, gaining even more traction as prices decline further.

The bears have officially retaken the $15.78 level. The VIX is trading flatter in the early premarket, currently at $13.86. With more “bullish catalysts” on the horizon, we’ll continue to wait on the sidelines in terms of future analysis until the data is more reliable and can paint a clearer picture for the road ahead. However, we stand by the analysis that $13 will be the most likely point that prices consolidate around.

II-II

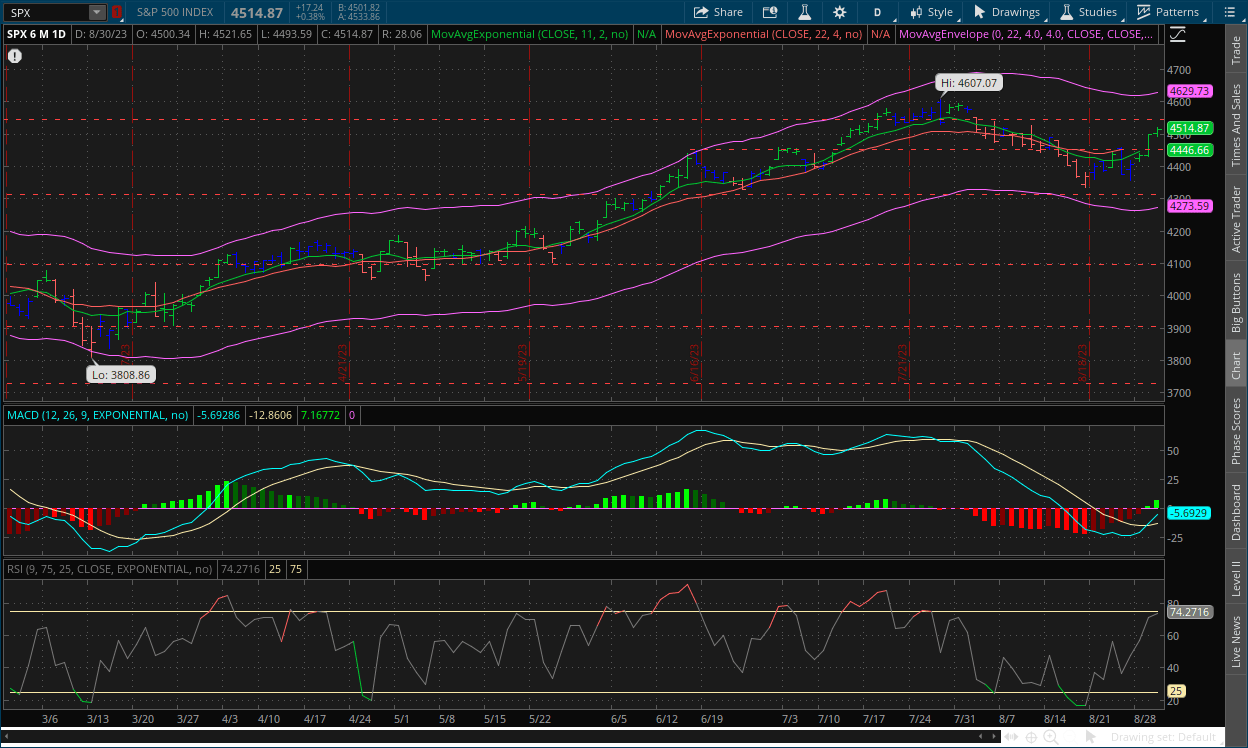

S&P 500: (SPX)

Wednesday Recap:

The S&P would open Tuesday’s session just above breakeven at $4,500, and work to a low of $4,493 early on. Prices would then climb the rest of the way, reaching a high of $4,521 before closing at $4,514.

Daily Chart:

Strength would move in favor of the bulls once again, showing strong momentum as they break back above the centerline while inertia would edge more in favor of the bulls again as prices continue to move higher.

The bulls have officially retaken the $4,450 level and now the $4,500 level as poor fundamental data is fueling the speculators. We were expecting this to happen as we’ve said, and with more potentially poor fundamental data on the horizon, this gives bulls more room to run. Read that sentence back and try to figure out that logic. But we still believe that the bears will take over once again sooner rather than later and reverse prices back to the downside as this is the signal we're getting from the weekly chart. This, along with the fundamentals being overall bearish (but bullish for speculators in the interim) for the economy, the S&P is still likely to flip.

III

Fundamentals:

III-I

ADP Employment Data for August:

Highlights:

|

Index: |

July: |

August: |

Wall Street Expectations: |

Take Five Expectations: |

|---|---|---|---|---|

|

Employment Change: |

371k(r) |

177k |

195k |

185k |

Private sector employment increased by 177,000 jobs in August compared to an upwardly revised 371,000 in July from 324,000. This month came in below both Wall Street and our own expectations.

Job stayers saw a year over year pay increase of 5.9% compared to 6.2% in July, the slowest growth since October of 2021. Job changers also saw pay growth decelerate to 9.5% year over year compared to 10.2% in July. For the first time, all 50 states and Washington D.C. experienced a year over year deceleration in pay growth.

Finer Details:

The goods producing sector saw only 23,000 job changers of the 177,000 total. Manufacturing took up the majority of the sector with 12,000 total, while construction and mining lagged compared to previous months, growing by 5,000 and 6,000 respectively.

Most of the changers came from the service providing sector, totaling 154,000. The bulk of the growth in this index came from education and health services (52,000), a data point that’s consistent with late stage labor cycle trends and something we’ve gone over before. Leisure and hospitality changers fell to 30,000 from July to August, marking the largest drop in the sector. Notably, financial activities services saw a total of 0 job changers, which is interesting considering the trend we’ve seen in financial services inflation.

Putting It Together:

The report on the private sector followed in similar fashion to the JOLTS data we reported on yesterday, i.e. the trend in the private sector is consistent with the notion that the labor market is tightening. Markets also took this as a bullish signal, as it gives the Fed less justification to hike interest rates again. But again, as we have said before, they’re ignoring the larger picture, a key characteristic of a speculative market.

When underlying fundamental data is coming in worse and worse, and the trends as well as historical context and data suggest it will continue to get worse, but markets are still rambling on, you have a speculative fueled market, i.e. market participants are buying out of greed and euphoria and not logic, a dangerous move on their part. But this is what usually happens, and it does not surprise us.

Tomorrow’s payroll data will be the key report this week however, which we will cover in Monday’s report. In the last report we covered, we said this: “Payroll gains tend to go negative extremely rapidly when heading into a recession. What we’ve been seeing with companies is they’ve been almost hoarding labor, and instead of expanding staff and hiring new workers, they’ve been using the excess cash to expand operations and give raises to the staff they already have. But if fear were to strike the markets, these gains again, can go away very very rapidly.” We’ll discuss this once again more in depth in Monday’s report.

IV

Market Psychology & Final Thoughts:

Futures are still higher as we head towards the open. The PCE report, the Fed’s preferred inflation measure, is on tap for today, with payroll gains, the unemployment rate, average hourly earnings and workweek scheduled for release tomorrow. As always, we hope you found this helpful, learned a thing or two, and have a great day.