The Take Five Report: 9/7/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: -0.70%

- Dow: -0.57%

- Nasdaq: -1.06%

- Russell 2k: -0.33%

U.S. indexes would open lower on the day once again, and prices would slide through most of the session, but would level off in the latter half of the day. Bond yields and oil futures continued to rise. MBA mortgage applications fell by -2.9% from a positive 2.3% the previous month while the S&P Global US Services PMI fell from 51.0 in July to 50.5 in August. The ISM Non-Manufacturing PMI however showed a positive read, jumping from 52.7% in July to 54.5% in August.

Asia:

- Shanghai: -1.13%

- Hong Kong: -1.34%

- Japan: -0.75%

- India: +0.58%

Asian markets slid in this morning’s session along with the rest of the global markets. China’s economic data continues to weaken, as trade exports fell by -8.8% and imports fell by -7.3%.

Europe:

- UK: -0.16%

- Germany: -0.19%

- France: -0.84%

- Italy: -1.24%

European stocks closed lower on Wednesday, weighed down by rising concerns about inflation due to high oil prices, slowing economic growth, and possibility of further monetary tightening by global central banks.

I-II

U.S. Sectors Snapshot:

- Communication Services: -0.54%

- Consumer Discretionary: -0.97%

- Consumer Staples: -0.19%

- Energy: +0.14%

- Financials: -0.17%

- Health Care: -0.61%

- Industrials: -0.48%

- Info Tech: -1.37%

- Materials: -0.33%

- Real Estate: -0.23%

- Utilities: +0.20%

II

Technicals:

II-I

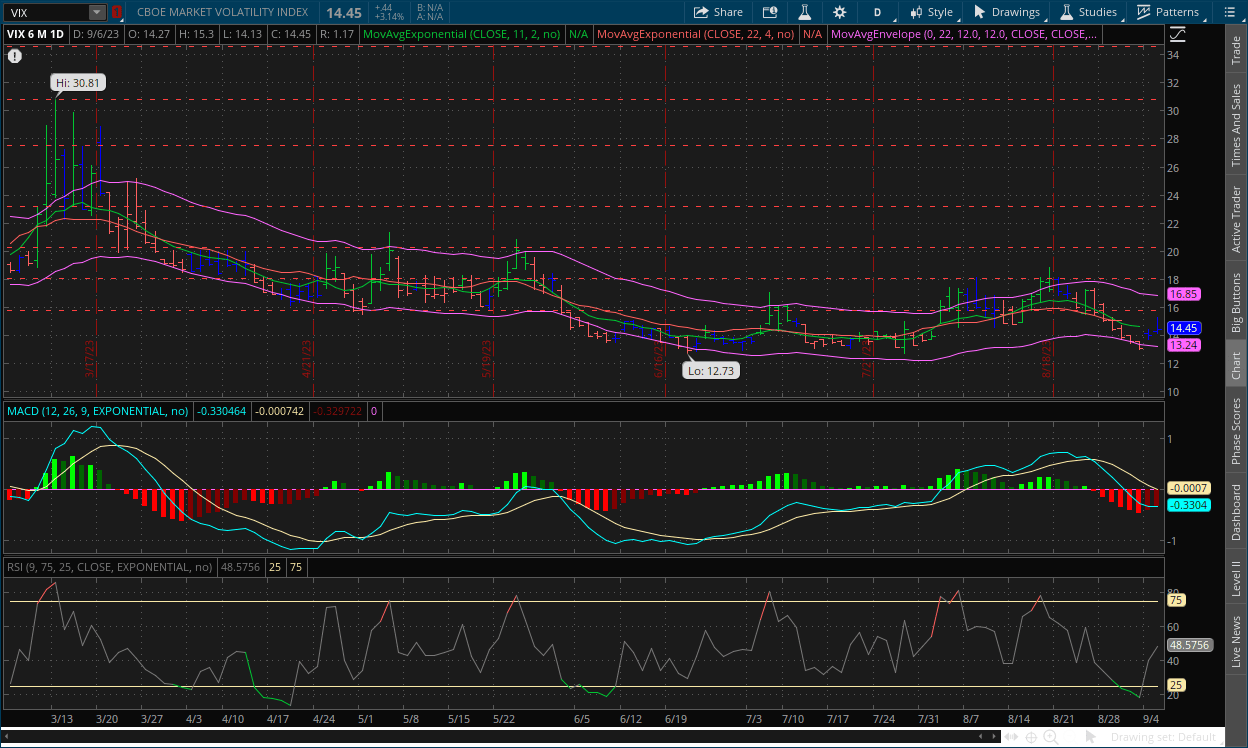

Volatility Index: (VIX)

Wednesday Recap:

The VIX would open Wednesday's session at $14.27, and work to a low of $14.13. Prices would climb to a high of $15.30 and would slide as markets began to level, ultimately closing near the open at $14.45.

Daily Chart:

Strength would move in favor of the VIX bulls for the second straight session, and look to continue their momentum as they make a push to bring price action back in their control. Inertia is still favoring the downside, but would continue to temper and flatten out a little more.

The VIX continued its bounce off of the $13 support level in yesterday's session, and prices next point of resistance will likely be at the $15 level. The VIX bulls now have momentum working in their favor, but a continued shift back to the upside in the MACD does not mean that prices will continuously follow with it. More consolidation is likely in store first.

II-II

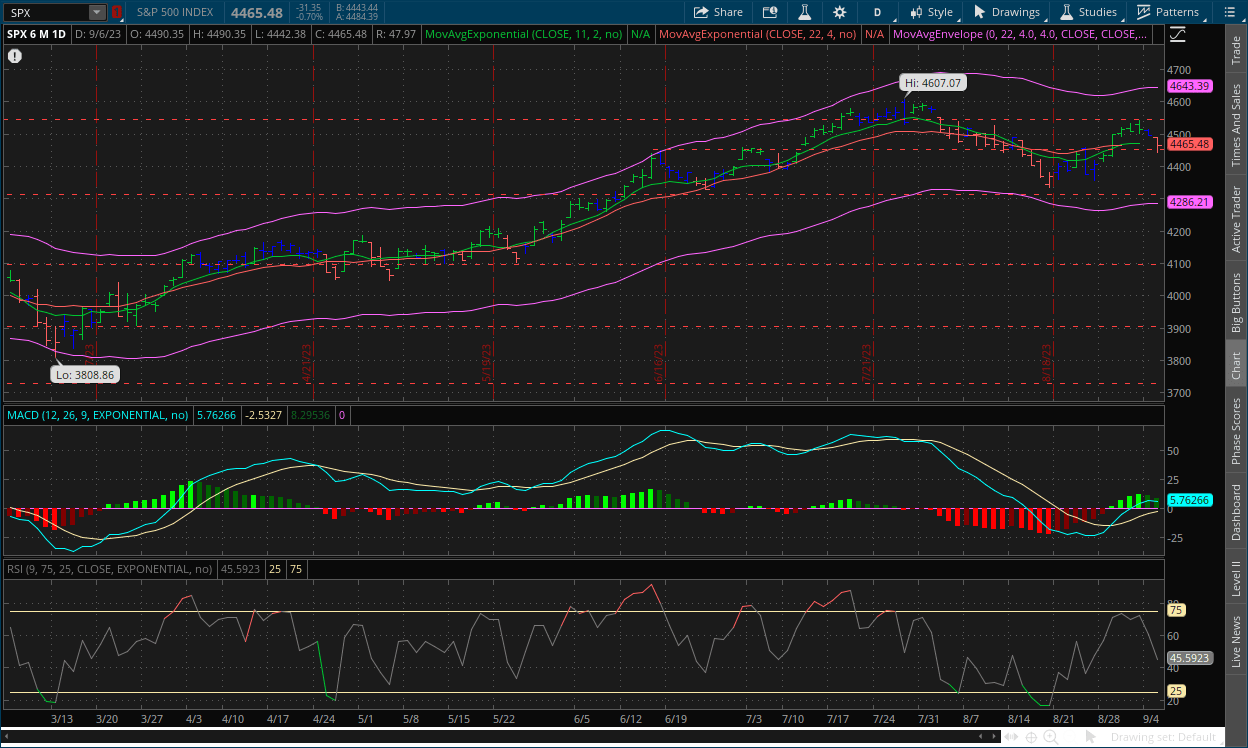

S&P 500: (SPX)

Wednesday Recap:

The S&P would open the day at $4,490, which also was the high of the session as bears came out of the gate firing. Prices would slide to a low of $4,442 before ultimately closing up from that point at $4,465.

Daily Chart:

Strength would move in favor of the bears for the second straight session, and will look to continue their momentum through the rest of the week and try to regain control of price action. Inertia would move more towards the downside as well and is flat but is on the cusp of a shift back in favor of the bears.

The bears now have momentum working back in their favor, but work will need to be done if they want to breakout below the $4,450 level, and like we said above, just because the bears have momentum in bringing strength back in their favor doesn't mean prices will follow continuously along with it, more consolidation is likely in store first.

III

Fundamentals:

III-I

Headlines:

1.) MarketWatch: Apple stock continues to decline amid worries about China’s reported ban on government iPhones

2.) MarketWatch: Investor allocation to gold is at its highest level in 11 years, JPMorgan strategist says

3.) Bloomberg: German industrial production down for third month as woes linger

4.) Bloomberg: China’s gold binge extends to tenth month as reserves climb

5.) Financial Times: China’s exports tumble as trade woes persist

III-II

Renewed Inflationary Concerns?

Oil Production Cuts Extended:

Saudi Arabia and Russia have agreed to extend oil production cuts by 1 million barrels per day and 300,000 per day respectively, until the end of the year. The production cuts have resulted in oil prices across the globe rising more than 20% since the first announcement was made back in May by the Saudi expanded OPEC (different from the Saudi nation) organization.

The international benchmark, Brent Crude, has settled above $90 per barrel for the first time since November of 2022, while the US’ West Texas Intermediate has settled above $87 per barrel. Prices at the pump here in the U.S. have risen to an average of $3.80, and have begun to be felt throughout the entire economy.

Russia likely extended production cuts due to weakening demand from China, who has seen their economy slow to a significant degree to say the least. Saudi Arabia, and in extension OPEC, want a floor price of at least $85 per barrel on Brent Crude. Their output has been reduced from 10.5 million barrels per day in April to 9 million, through a combination of OPEC mandated targets and their own voluntary cuts. This latest announcement means their output will remain at 9 million barrels per day until the end of December, which is 25% lower than their maximum capacity.

Inflationary Concerns:

We’ve gone over and discussed in previous reports regarding CPI and PPI that inflationary pressures pertaining to energy were still prevalent, and in the case of oil companies, shorter term rises in profits were likely on the horizon due to sliding global demand as well as likely extended cuts by OPEC and other leading oil producers, in which most reside within BRICS.

Many economists were taken aback by the extended cuts, but this was something we expected and factored in. We looked at the geopolitical landscape specifically, and the question boiled down to this: From their point of view, why wouldn’t they extend and/or increase production cuts? To put it *extremely* simply, it helps strengthen their own economies by raising oil prices while simultaneously reducing how much they actually have to produce (making it easier on them) and helps weaken their geopolitical rivals (i.e. the West), at least in the short-term because this also could blow up in their face if demand were to weaken in the future.

The rise in oil prices will prove challenging for central banks across the globe, as they now have to factor in a decreased supply of oil for the remainder of the year as well as the worry of de-anchoring inflation expectations. This is especially concerning as we head towards the winter months as well, where demand for the commodity is usually higher. Oil as we know runs the world. Energy is the backbone of every economy. If oil prices continue to rise, increased inflationary pressures will be felt in other areas, e.g. airlines, transportation and freight, utilities, manufacturing, the list goes on. As a final noteworthy point, the ISM non-manufacturing report, which is a measure of services in the US economy, contained another eye opener in one of its sub indexes following its release yesterday. The prices paid level, rose from 56.8 to 58.9. This is significant because it relates to the services component of CPI, which takes up the majority of it, and the ISM index is something economists use to help make their projections.

IV

Market Psychology & Final Thoughts:

Markets are heading for another low open as futures continue to fall while yields and oil futures rise. Market participants are worried about de-anchoring inflationary expectations, and that inflation as a result will rise after so much progress has been made, causing central banks to raise rates even higher and keep them higher for longer. As always, we hope you found this helpful, learned a thing or two, and have a great day.