The Take Five Report: 9/11/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: +0.14%

- Dow: +0.22%

- Nasdaq: +0.09%

- Russell 2k: -0.23%

U.S. markets would open Friday’s session on a positive note, and would bounce up and down through the first half. However, the second half took a turn, and prices slowly slid until the final minutes, where bulls bought the dip and propelled the three major indexes to a positive finish. Consumer credit growth slowed this month to $10.4B, from $14B the previous month. Revolving consumer credit grew to a total $1.271T, while non-revolving grew to $3.714T.

Asia:

- Shanghai: +0.84%

- Hong Kong: -0.58%

- Japan: -0.43%

- India: +0.79%

Asian markets were mixed in this morning’s session, with Hong Kong sliding following Friday’s closure due to bad weather, and Japan after BOJ Governor Kazuo Ueda said over the weekend that the central bank could end its negative interest rate policy when the 2% inflation target is sustainably achieved. Adding that the BOJ could have enough data by the end of the year to determine whether it can proceed with policy changes. China’s CPI came in at 0.1%, while its PPI came in at -3.0%.

Europe:

- UK: +0.49%

- Germany: +0.14%

- France: +0.62%

- Italy: +0.28%

European markets closed higher on Friday, breaking a seven-session losing streak that started the week prior. German CPI came in slightly lower at 6.1%. Industrial production in Spain dipped by -1.8%, the fourth straight month with a decline while France saw its industrial production rise marginally at 0.8%.

I-II

U.S. Sectors Snapshot:

Communication Services: +0.35%

Consumer Discretionary: +0.03%

Consumer Staples: +0.16%

Energy: +0.97%

Financials: +0.24%

Health Care: -0.04%

Industrials: -0.46%

Info Tech: +0.21%

Materials: +0.12%

Real Estate: -0.63%

Utilities: +0.96%

II

Technicals:

II-I

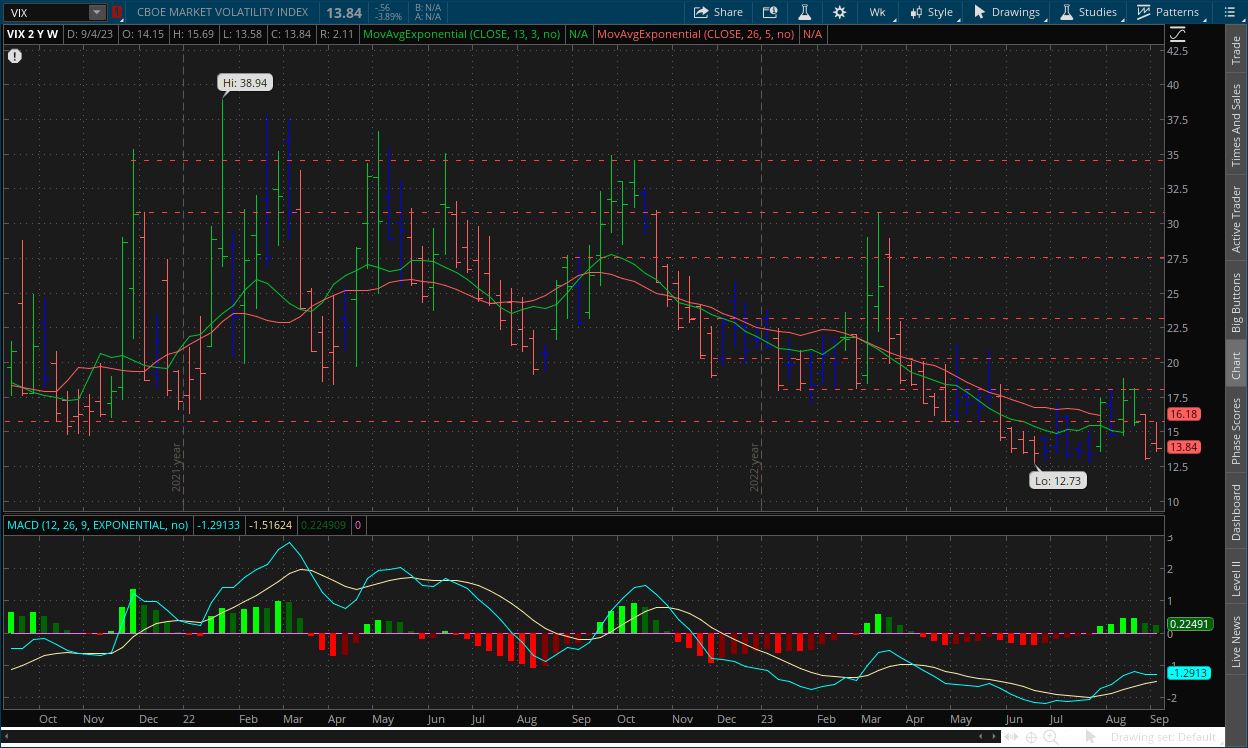

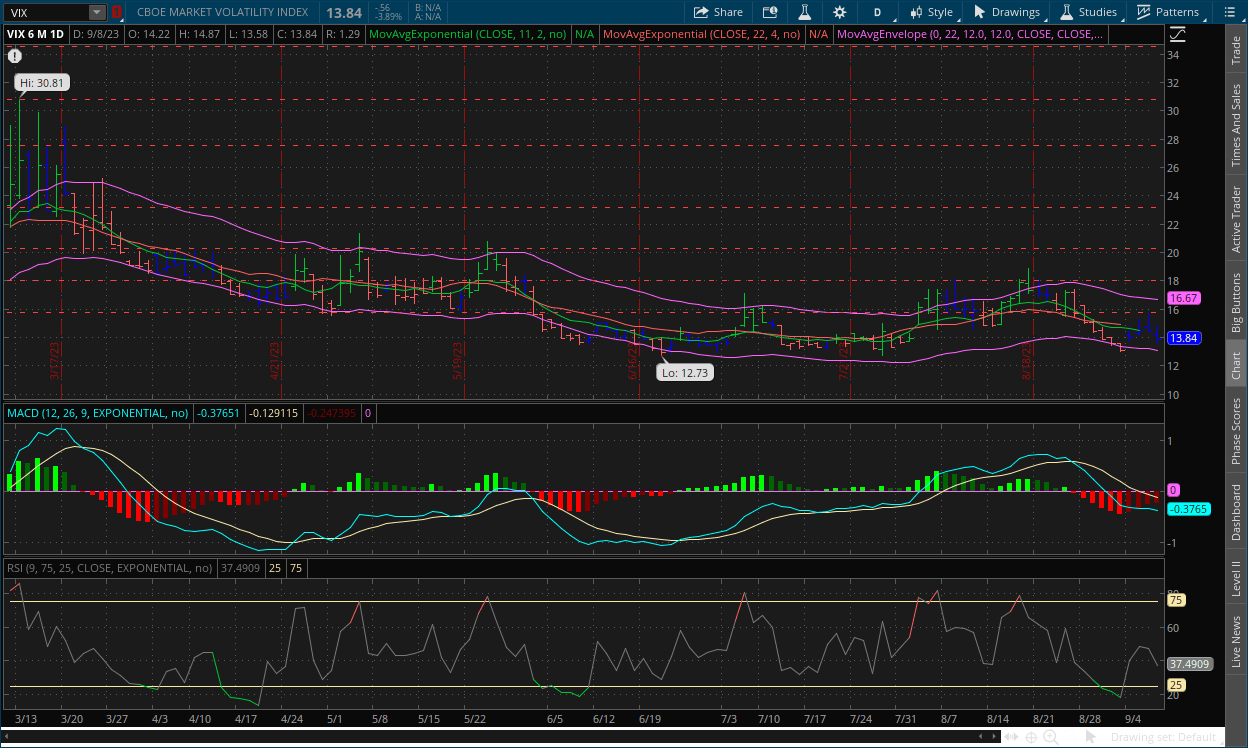

Volatility Index: (VIX)

Weekly Chart:

The VIX would start the week higher than the previous at $14.15 and would climb steadily throughout the week and reach a high of $15.69. Prices during the final stretch of the week would fall however, reaching a low of $13.58 and ultimately close the week at $13.84.

Strength decreased in favor of the VIX bears for the second straight week following the activation of the triple bullish divergence almost two months ago as the VIX bulls are losing their steam. Inertia would move more to the downside as well after the marginal rise following the activation. The divergence, despite the implied strength of the signal, has achieved minimal results. This is typical in securities that are downtrending for a long period of time. They consistently trace divergences on the way down, and following an activation they only rise for a short period of time before continuing they’re downtrend. The VIX differs from other securities though, i.e. it measures volatility and not “valuation”. Meaning its price action is usually flatlined for extended periods of time, rapidly rises to peak levels, and swiftly drops back down to previous points of support. The technical signals are showing that with each cycle below the centerline, the VIX bears (i.e. market bulls) are getting weaker, and eventually their grip will loosen. But the question is when, and for how long?

Daily Chart:

Despite the drop in prices, strength would still move in favor of the VIX bulls, albeit slightly, as they continue to make their push back towards the centerline. Inertia on the other hand would continue to fall in favor of the VIX bears, but its slope has tempered from the prior week. It looks as if VIX prices will be heading for another consolidation period between $13 and $15. As for its extent, it could be short lived if any of the catalysts this week shatter expectations.

II-II

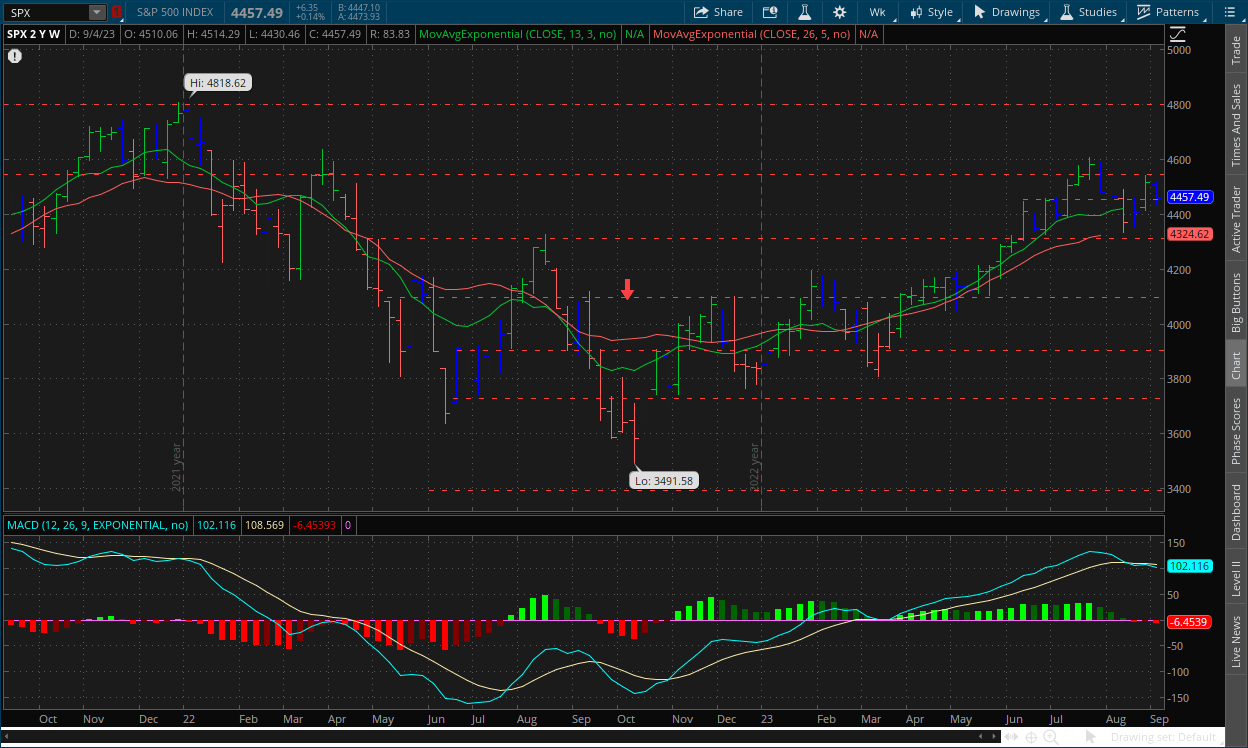

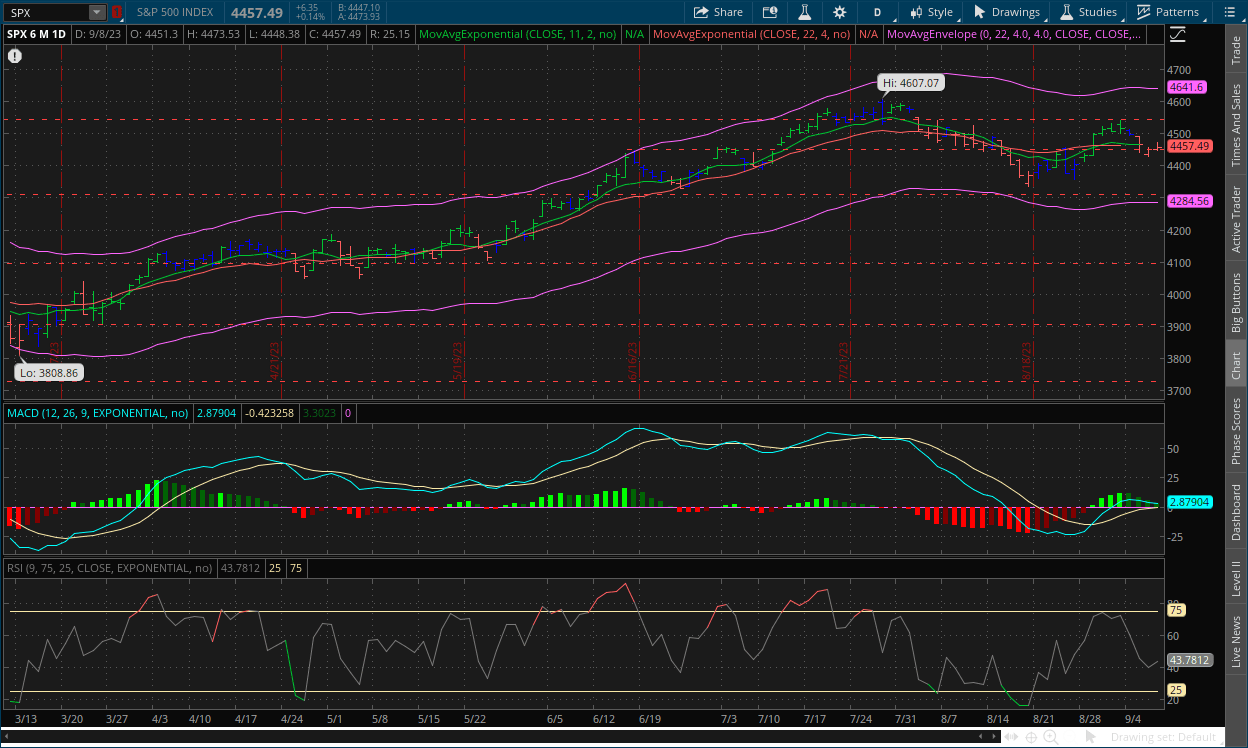

S&P 500: (SPX)

Weekly Chart:

The S&P following last week’s rally saw another decline, opening the week at $4,510 and working to a high of only $4,514 before sliding to a low of $4,430. Prices would close the week just above the $4,450 level at $4,457. Strength would move in favor of the bears and keep the slight ground they have on the bulls. Inertia would temper to the upside a little bit, but still remain with an upward slope.

The bears managed to stay afloat beneath the centerline in the prior week. However the moves they’ve been making in the grand scheme of things have been weak. They are due for some kind of run, and the market is due for a minor correction at the *very least* at some point, and we believe that it will come sooner rather than later.

Daily Chart:

Strength moved in favor of the bears in Friday’s session despite the positive finish, however inertia would remain flatlined overall. Prices managed to break below the $4,450 level on Thursday, but this is likely to be a false downside breakout following Friday’s subsequent rise and with futures heading up in premarket trading. The bears made some decent ground in August, but these last two weeks have swiftly destroyed all that ground. A large part of it has to do with speculative behavior, and questionable logic, i.e. reacting euphoric to increasingly poorer fundamental data not just domestically, but globally as well. It will no less be interesting to see the dynamic play between bulls and bears play out this week as well, as there are more speculative catalysts for both parties to overreact to.

Our outlook remains the same however as we said above, the bears are due for some kind of run. The near-term fundamental and technical signals support speculative psychological behavior, which is what's driving prices up, but the longer-term analysis of the two forces is showing weakness in the current trend, giving the bears an edge over the bulls going forward, allowing the psychology of the crowd to shift at one point or another.

III

Fundamentals:

III-I

Headlines:

1.) Bloomberg: China’s economy shows tentative signs of stability as CPI ticks up

2.) Wall Street Journal: India spends big on what it needs most to catch up to China

3.) Wall Street Journal: Earnings estimates are rising, a welcome sign for 2023 market rally

4.) Financial Times: China gives strong warning against bets on renminbi depreciation

III-II

The Week Ahead:

United States:

CPI & PPI:

|

Index: |

Prior: |

Wall Street Expectations: |

Take Five Expectations: |

|---|---|---|---|

|

Headline CPI: |

0.2% |

0.6% |

0.7% |

|

Core CPI: |

0.2% |

0.3% |

0.3% |

|

Headline PPI: |

0.3% |

0.4% |

0.5% |

|

Core PPI: |

0.3% |

0.2% |

0.3% |

Our view on the CPI and PPI releases this week is closely in relation to that of Wall Street’s, although we do expect them to come in a little hotter than their consensus forecast. Oil production cuts from the globe's major oil producers have been sending futures contracts on the commodity higher and higher, resulting in higher prices at the pump. This will likely be the bulk of the increase, and will continue to rise even further for the October release that covers September.

Higher oil prices will also affect other areas like airlines, shipping and freight, transportation, utilities, etc. Weather also will play a key role in food pricing, as well as in utilities services and construction indexes, among others. Services will be the key area to look out for, as this is where the Fed will be paying the most attention.

Retail Sales:

|

Index: |

Prior: |

Wall Street Expectations: |

Take Five Expectations: |

|---|---|---|---|

|

Retail Sales: |

0.7% |

0.2% |

0.3% |

|

Core Retail Sales: |

1.0% |

0.4% |

0.4% |

We expect consumer spending to temper a bit compared to last month's increase, with higher gas prices eating into this metric. We would be shocked if the reading came in above 0.4%, and we’re inclined to believe the Fed would be as well. If demand doesn’t weaken all that much and inflation heats up, rate hike expectations for the November meeting may become the consensus.

Industrial Production & Capacity Utilization:

|

Index: |

Prior: |

Wall Street Expectations: |

Take Five Expectations: |

|---|---|---|---|

|

Industrial Production: |

1.0% |

0.2% |

0.3% |

|

Capacity Utilization: |

79.3% |

79.3% |

79.4% |

The prior report exploded to 1.0% after high temperatures and weather effects saw utilities output surge 5.4%, which paced the increase. Expect this report to be nowhere near the previous, although we still do expect it to come in above Wall Street’s expectations.

China:

Some of the key data coming out of China this week has already been released, with the CPI increasing 0.2% and the PPI decreasing -3.0%, which both were in line with expectations. Other key releases that were released this morning, those being new yuan loans and the M2 money supply figures, which saw the M2 increase 10.6% year over year and new yuan loans jump to 1.36 trillion renminbi from 345.9 billion renminbi last month, showing China is doing everything they can in terms of providing stimulus in order to halt their economy and currency from falling further than it already has.

On Friday, they’ll be releasing the housing prices index, industrial production, retail sales, and unemployment rate for August, with both retail sales and industrial production expected to show a slight improvement. Market participants should be keeping a close eye on the youth unemployment rate after July’s figure was temporarily suspended by the NBS without any clear timeline for the suspension. This is a key area of concern for the nation as a whole, as the youth unemployment rate is at a staggering 21.3% as of June, around four times more than the national unemployment rate of 5.3%.

India:

Inflation and balance of trade for August will be in focus for this week. Inflation data is being released on Tuesday, with expectations having the report dip slightly to 7% year over year from 7.44% in July, the highest since April of last year. Balance of trade will be released on Friday, with expectations for the deficit to widen slightly to -$21 billion. India has been seen reducing exports across some of their major commodities, specifically rice, as this has taken an effect on their deficit.

Japan:

The Reuters Tankan index on manufacturers’ sentiment will be released on Wednesday, after a big jump to +12 in August (its highest recorded level this year), sentiment is expected to temper slightly to +10 for September. The PPI for August will be released on Wednesday as well, with this expected to temper as well with 3.2% year over year expected compared to 3.6% in the prior month. Machine orders are also expected to decline, with -10.7% expected this month following a -5.8% decline in the prior report.

Eurozone:

The ECB meets this week, and it’s not clear at this point in time what decision they’ll come to, i.e. whether to raise or hold rates. Markets have priced in about a 65% chance for a hold, which may signal the end of the tightening cycle, although the ECB would never suggest that at this point even if they do pause. There’s still a good chance they raise rates one more time, but ultimately it will come down to their projections for inflation moving forward.

United Kingdom:

This is potentially a big week for the UK ahead of the next monetary policy meeting. The BOE this past week hinted that the decision is in the balance and not a foregone conclusion that many expect. Markets are pricing in a 70% chance of a hike and more than a 50% chance of another after that by February. The labor market report on Tuesday will likely be significant, as further slack could provide some ease in their state of mind. The GDP estimate on Wednesday could also be interesting, all depending on where the estimates are.

IV

Market Psychology & Final Thoughts:

Futures are still on the rise with oil prices falling and bond yields tempering to start the week. In terms of US catalysts, there isn’t much until Wednesday, giving the bulls a path to run. Later this week will prove interesting though, as there will be many key reports and events markets will be paying attention to. As always, we hope you found this helpful, learned a thing or two, and have a great day.