The Take Five Report: 9/14/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: +0.12%

- Dow: -0.20%

- Nasdaq: +0.29%

- Russell 2k: -0.78%

U.S. markets would close mixed overall following the release of the CPI data prior to market open. Indexes remained steady, and slightly rising through a good portion of the session, but began to slide rapidly around 2:00, bringing them all into the red heading towards the close. A small rally in the final minutes helped the S&P and Nasdaq edge out gains. Small cap selloffs paced the major indexes, with the Russell 2000 sliding -0.78%.

Asia:

- Shanghai: +0.11%

- Hong Kong: +0.21%

- Japan: +1.41%

- India: +0.08%

On Wednesday, Asian markets fell across the board following the release of the Reuters Tankan poll (which we discussed on Monday). It showed that corporate confidence in Japan fell this month among both manufacturers and non-manufacturers, sliding from +12 to +4 among the former, with the latter dropping -9 points to +23. Japan’s wholesale inflation fell to 3.2% year over year, while India’s inflation rate eased significantly from 7.44% to 6.83% in August. This morning, Asian equities rebounded following the hot U.S. CPI read.

Europe:

- UK: -0.02%

- Germany: -0.39%

- France: -0.42%

- Italy: -0.33%

European markets would close largely lower in yesterday’s session, after investors digested new eurozone industrial production data, which saw output fall -1.1% month over month. Elsewhere data showed the UK economy slid at the fastest pace in seven months, with real GDP falling -0.5% in July, offsetting the 0.5% increase in June. European markets are marginally down this morning, with the exception of the UK, through the first half of their session.

I-II

U.S. Sectors Snapshot:

- Communication Services: +0.40%

- Consumer Discretionary: +0.90%

- Consumer Staples: +0.26%

- Energy: -0.76%

- Financials: -0.10%

- Health Care: +0.02%

- Industrials: -0.67%

- Info Tech: +0.31%

- Materials: -0.59%

- Real Estate: -1.03%

- Utilities: +1.20%

II

Technicals:

II-I

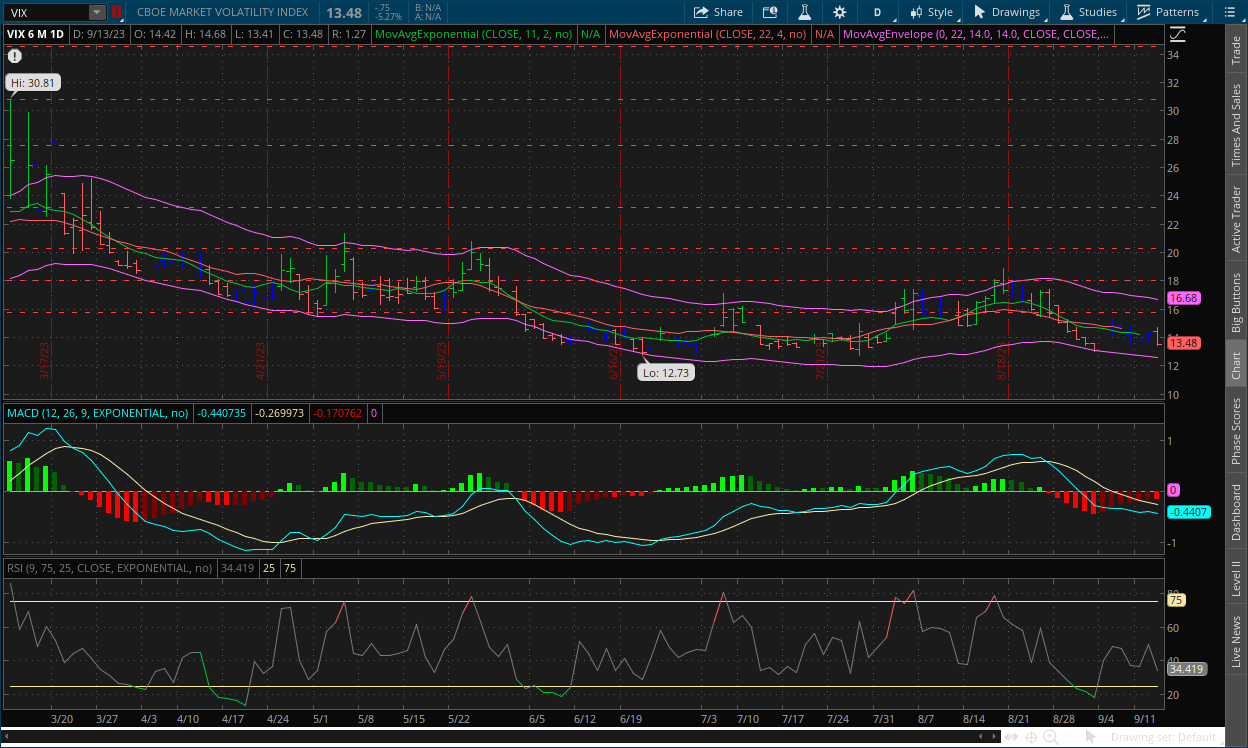

Volatility Index: (VIX)

Wednesday Recap:

The VIX would open yesterday’s session at the high end of the consolidation range at $14.42, and would reach a high of $14.68. Prices however would slide throughout the day, reaching a low of $13.41 before closing at $13.48.

Daily Chart:

Strength would move in favor of the VIX bears, snapping a six-session winning streak for the opposing party, who have kept good momentum in their fight to recapture the centerline. Inertia would remain in slight favor of the VIX bears and is still flatlined overall.

The VIX has returned to its consolidation range of $13-$15 over the last two weeks or so. Prices have managed to break above $15 twice, but have failed to fall below $13, with the lowest mark being $13.02. The VIX bulls have decent momentum heading towards the centerline (as the bears do on the S&P), but given the little price action, a move back above may prove weaker unless they make strides. As of right now, the markets have their eyes set on the PPI release and retail sales report. They didn’t move all that much following the CPI, but that was likely them expressing some form of patience and waiting for these other two releases to get a bird's eye view of them all.

II-II

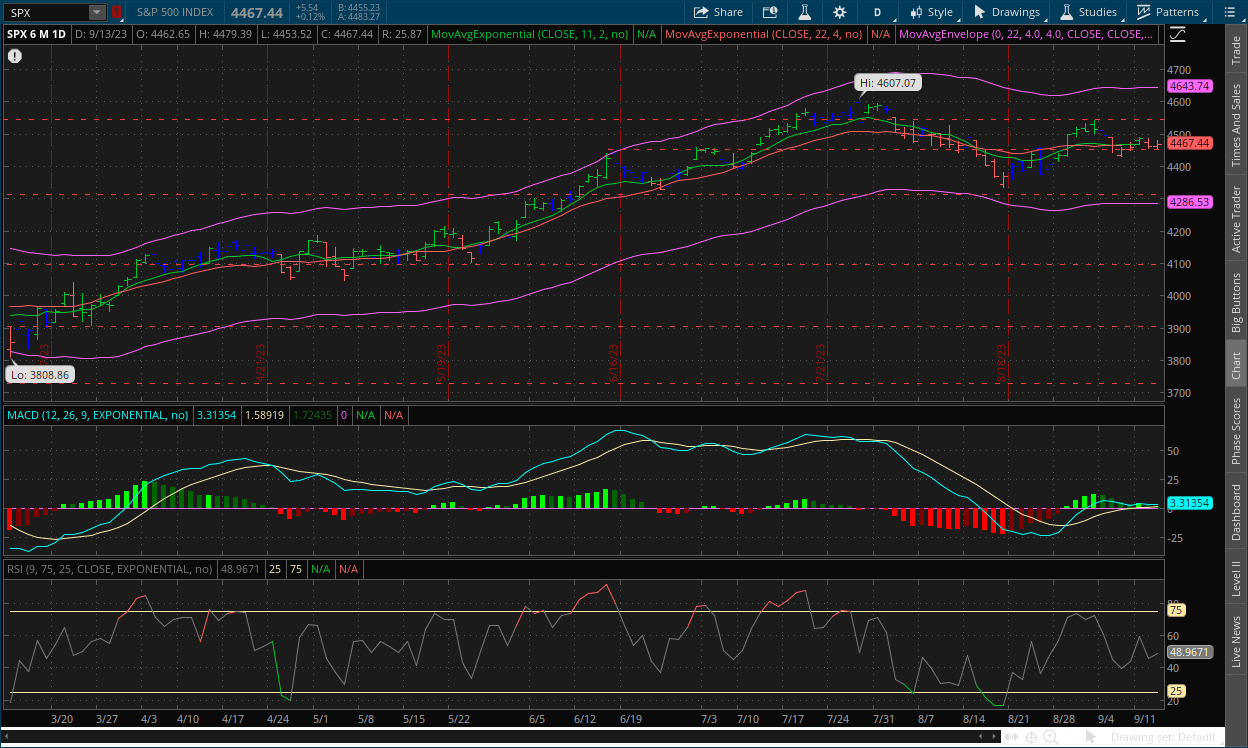

S&P 500: (SPX)

Wednesday Recap:

The S&P would open the session at $4,462, and reach a high of $4,479. Prices would fall to a low of $4,453 in the final hour, before rallying from that point and closing at $4,467.

Daily Chart:

Strength would move in favor of the bears as they continue their bid to regain control of the centerline. Inertia is still edging slightly in favor of the bears, but is nearly dead flat.

The S&P’s price action over the last few days has remained minimal, despite the bulls having some room to move. Both parties seem to be cautious, volume has slipped over the last few days as well, showing more participants remaining on the sidelines. As prices continue to consolidate, the MACD-H will continue moving in favor of the bears, although it will be weaker unless they can make a strong break below the $4,450 level, which will likely be caused by a fundamental catalyst, e.g. hot PPI and retail sales readings. MACD Lines are also substantially weaker compared to their previous peak, despite prices nearly rising back to highs. As we said in our previous report, the bears have a window of opportunity approaching.

III

Fundamentals:

III-I

Headlines:

1.) MarketWatch: ‘Emerging markets have a China problem.’ This strategist favors India, which just hit a record

- T5 note: The reason we highlight this is because India is a market that we hold more in favor of than China or any other in the East for that matter

2.) MarketWatch: Leaked inflation forecast turns ECB expectations toward a hike

- T5 note: ECB ends up hiking rates by 25 basis points

3.) Bloomberg: China cuts reserve requirement ratio for second time this year

4.) Markets Insider: US commercial real estate crisis deepens with office vacancy rate topping 2008 highs to hit a new record

5.) Fox Business: Jamie Dimon warns risks to US economy: ‘We’ve been spending like drunken sailors’

6.) Financial Times: Private capital sector too complacent about risks, says global regulatory body Iosco

III-II

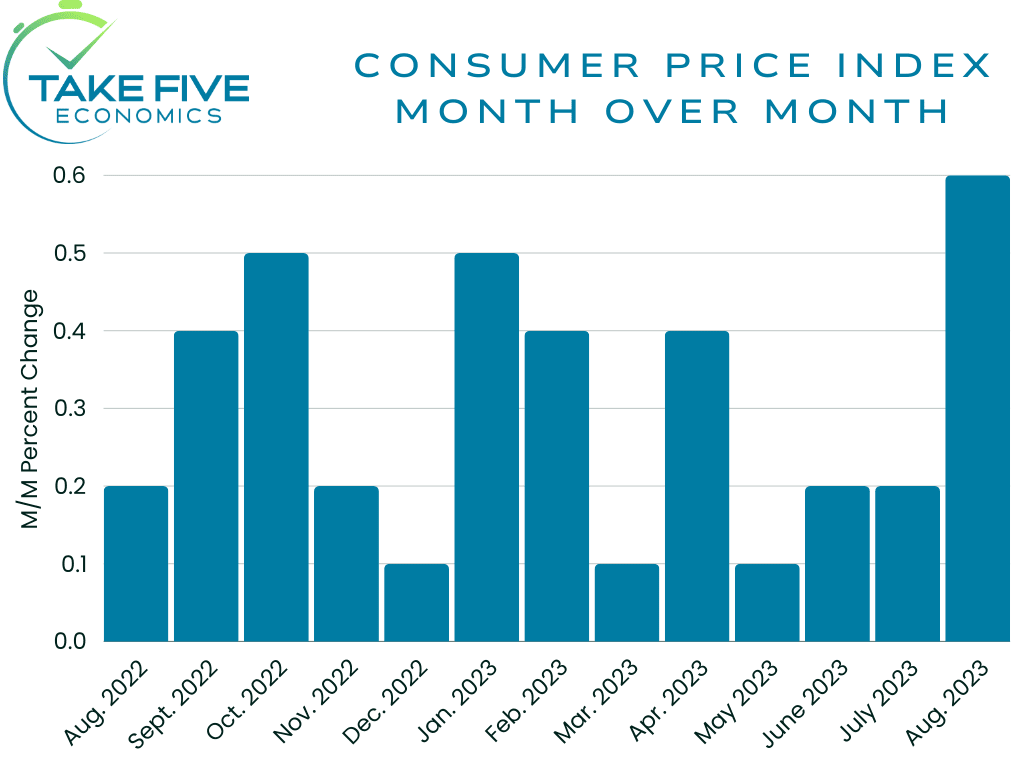

August CPI Data:

Highlights:

|

Index: |

July 2023: |

August 2023: |

Wall Street Expectations: |

Take Five Expectations: |

|---|---|---|---|---|

|

Headline CPI: |

0.2% |

0.6% |

0.6% |

0.7% |

|

Core CPI: |

0.2% |

0.3% |

0.2% |

0.3% |

Month over Month:

Headline CPI increased 0.6% month over month, the largest increase in 14 months, which matched Wall Street expectations and was slightly below ours. Core CPI rose 0.3%, matching our expectations but coming in slightly higher than Wall Street’s.

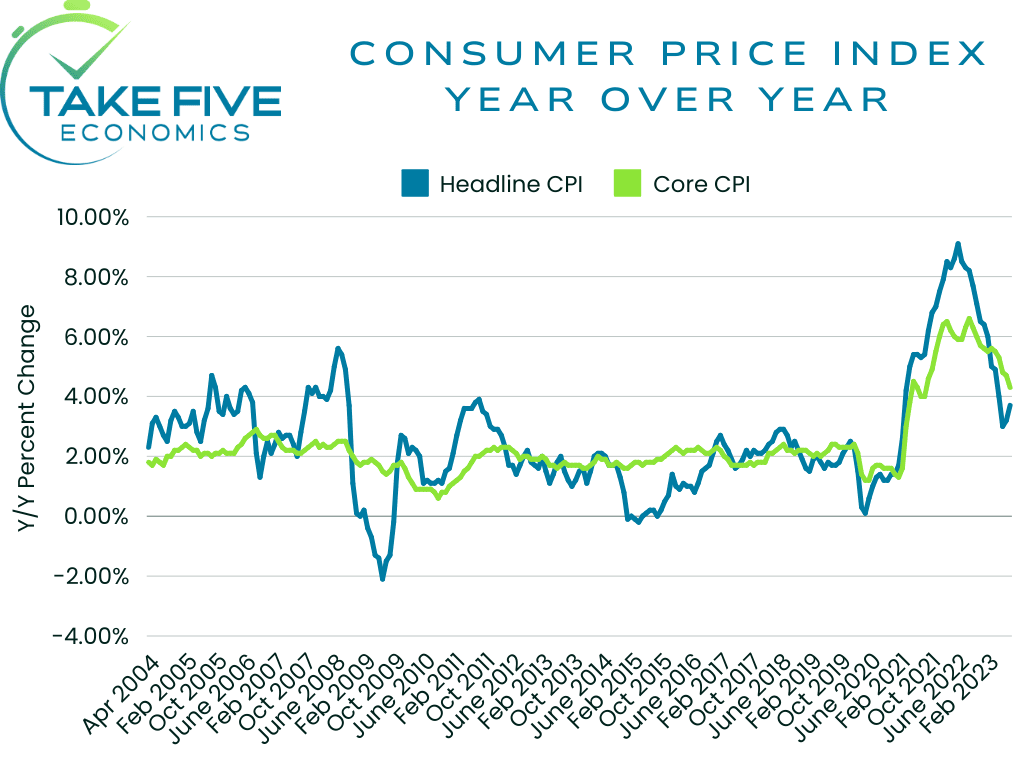

Year over Year:

Headline CPI was up 3.7% on a year over year basis compared to 3.2% in July, while core CPI moved downwards, from 4.7% in July to 4.3% in this release.

Finer Details:

The Rise in Energy Costs, Its Effects, and Our Outlook:

The index for energy was the largest contributor to the monthly increase and accounted for over 50% of it. Energy rose 5.6% in August with all of the major components within the index increasing as well. Energy commodities, i.e. gasoline and fuel oil rose by 10.5%. Energy services rose as well, with electricity headlining the increase there, but the energy services index as a whole rose at a much more marginal pace.

In Monday’s report, we said that energy would likely contribute the most to a hot reading. Production cuts by the globes major oil producers (i.e. OPEC, Saudi Arabia, and Russia) were the main catalyst for the spike, and it has finally been reflected truly within the report. Prices will likely continue to rise in the coming months, but slowing demand has also been a key issue to look out for as this is one of the main reasons why production cuts have been enacted. This could be looked at as more speculative, but it's too early to tell right now from what we can see.

The rise in energy costs have already begun to affect, and will continue to affect other key areas moving forward as many industry groups will have to prepare for higher input costs, and will likely raise their own prices to protect margins. In this report, we saw a rise of 2.0% in transportation services compared to 0.3% the month prior, airline fares saw a rise of 4.9% compared to a -8.1% decline in the previous two reports, delivery services rose 2.5% compared to a -0.7% decline last month, among others. Other industries such as manufacturing, shipping and freight, utilities, etc. will be reflected in the PPI reports.

Current projections show that the oil supply deficit is about -1.8 million barrels less than what is required for daily demand, and that the deficit is set to widen to -3.3 million barrels per day by the end of the year, which would be the largest global deficit since 2008. This amount of tightening of the global supply chain will no doubt send prices back around $100 per barrel if global demand stays at current levels, and prices at the pump over $4 again (which we’re already almost there) in terms of the national average, as some areas will be higher than others (we're looking at you California). But again, we ask the question of will demand stay the same, rise, or decrease even further in order to balance price stability?

Food:

The food index rose 0.2% in August, as it did the previous month as well. The six major grocery store food group indexes were split over the month, with three increases and three decreases. We expected a larger rate increase within food, around 0.4% but we’re obviously happy that we didn’t. However we do expect the rate to climb higher in the following reports, but perhaps not as strongly as we may have thought.

Core CPI (All Items Less Food and Energy):

The shelter index was the largest contributing factor within core CPI, which advanced for the 40th consecutive month, accounting for over 70% of the increase. Rents still haven’t begun to rollover, as the index rose 0.5% in August with owners’ equivalent rent rising 0.4%. Insurance costs also rose again as we’ve been seeing reflected in prior reports as well as PPI, with motor vehicle insurance rising 2.4% compared to 2.0% last month. Medical care also ticked up 0.1% compared to either declines or flatness in prior months. This will likely continue to marginally rise as we’ve seen medical facilities hire more and more staff in the latest labor market reports.

IV

Market Psychology & Final Thoughts:

Futures are rallying rather significantly as we head towards the open. The CPI didn’t affect markets all too much despite the hot read. But as said above, our theory is that markets are likely expressing *some* patience, and waiting for the release of the PPI and retail sales reports (which we will cover tomorrow) in order to gain a bird's eye view of them all. The CPI alone will increase expectations for the Fed to raise rates in the November 1 meeting, and our expectation is that PPI comes in hot as well, but with a more tempered retail sales. As always, we hope you found this helpful, learned a thing or two, and have an incredible day.