The Take Five Report: 9/19/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: +0.07%

- Dow: +0.02%

- Nasdaq: +0.01%

- Russell 2k: -0.69%

US indexes would open the day at the breakeven mark, and hover around that point for the first hour or so before rallying through the middle portion of the session. Prices would encounter resistance there however, and wind up sliding towards the final stretch and would finish with marginal gains slightly above breakeven.

Asia:

- Shanghai: -0.03%

- Hong Kong: +0.37%

- Japan: -0.87%

- India: -0.36%

Asian markets mostly fell in this morning’s session as market participants digested the Australian central banks’ minutes from its policy meeting on September 5th where the bank had said that inflation in the country is still “too high.” The bank had said that further policy tightening may be required if inflation is more persistent than expected.

Europe:

- UK: -0.76%

- Germany: -1.05%

- France: -1.39%

- Italy: -1.07%

European markets closed largely down in yesterday’s session as market participants got the central bank jitters once again. Europe has been all over the place as of late. Fundamental reports are showing economies trending more towards stagflation, i.e. low or negative economic growth, poor labor market mixed with higher inflation. Their data at the current moment in time is not as headline happy as the US’, and more investors are growing concerned with the trends happening across the pond.

I-II

U.S. Sectors Snapshot:

- Communication Services: +0.27%

- Consumer Discretionary: -1.01%

- Consumer Staples: +0.08%

- Energy: +0.68%

- Financials: +0.31%

- Health Care: -0.18%

- Industrials: +0.11%

- Info Tech: +0.47%

- Materials: -0.43%

- Real Estate: -0.81%

- Utilities: -0.05%

II

Technicals:

II-I

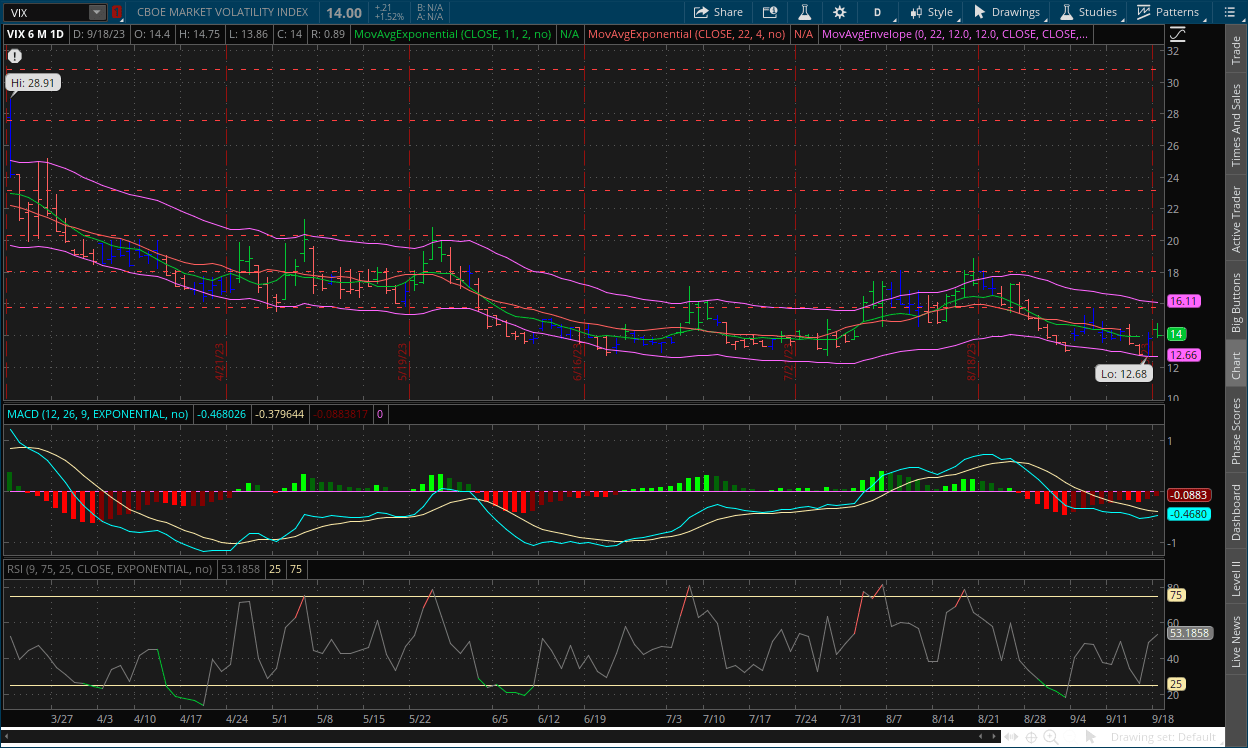

Volatility Index: (VIX)

Monday Recap:

Following Friday’s bounce up to $13.79 at the close, the VIX would open Monday’s session higher at $14.40, and work to a daily high of $14.75 before sliding in the middle part of the day. Prices would reach a low of $13.86 before closing at $14.

Daily Chart:

Strength once again moved in favor of the VIX bulls as they make their bid back towards the centerline, following the brief plummet experienced last week. Inertia is edging in favor of the bulls as well but is still overall downward.

The VIX’s breakout below $13 turned out to be a false one, as said on Friday: “Volatility decreased in markets on a day where higher volatility was implied following the hotter than expected PPI and retail sales reports. This may be looked at as a final push from the VIX bears (i.e. market bulls) in this cycle. This would mean the breakout below $13 would be false.” The VIX however continues to trade within its now trading range of $13-$15. There have been false breaks at the top end and the low end, but as we said yesterday, a reversal seems imminent. The $15 will be a key test for the VIX bulls. If they can break above it, they have the green light.

II-II

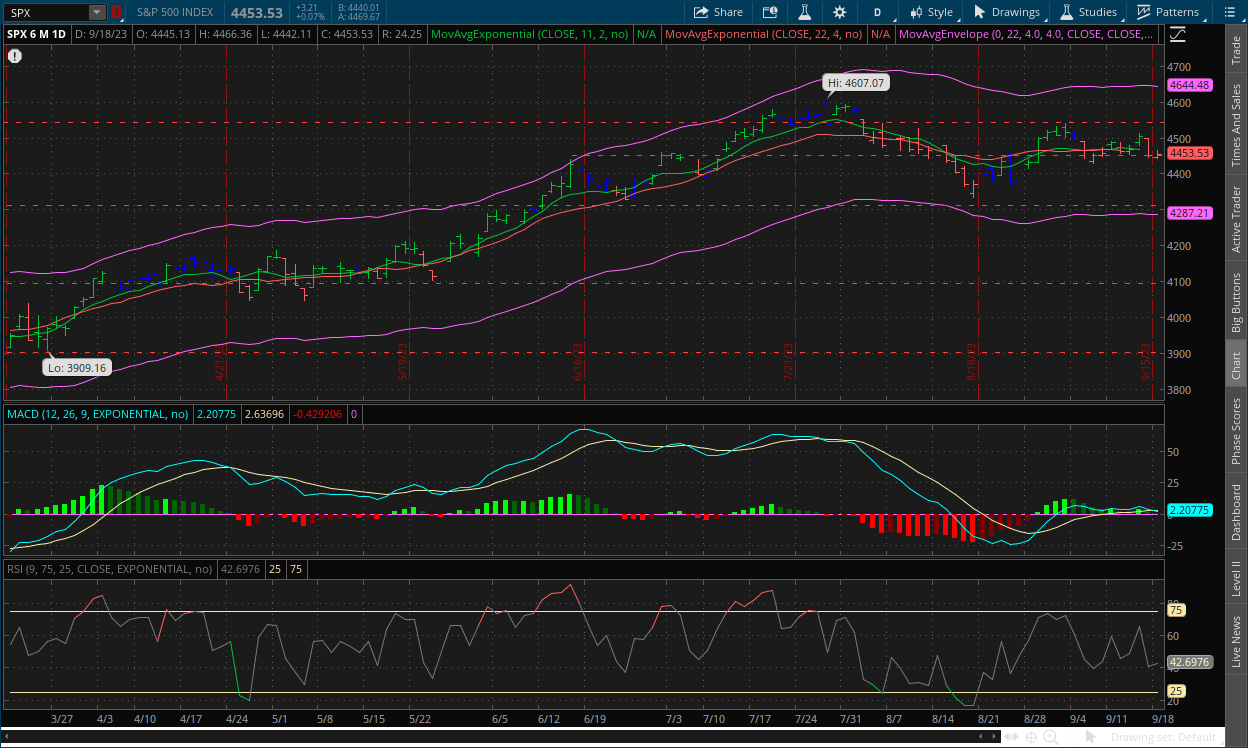

S&P 500: (SPX)

Monday Recap:

Following Friday’s fairly large decline, the S&P’s price action would temper in comparison. Opening the day at $4,445 and reaching its lowest point of only $4,442 shortly after the opening bell. Prices would reach a high of $4,466 before ultimately sliding back towards the breakeven mark and closing at $4,453.

Daily Chart:

Strength moved in favor of the bears, and they officially retook the centerline albeit by less than a sea hair. Inertia is tilting in favor of the bears as well, but remains flat overall.

The bears may have retaken the centerline, but they have yet to fully break below the $4,450 support level. Similar to the VIX bulls and the $15 resistance level, the $4,450 level is the key level the bears will need to break. After that, they have the red light, so to speak. We stand by our analysis that a market shift is on the horizon. The technical and fundamental forces are moving in a bearish direction, meaning the psychology will follow at some point. It's just that greed is a much harder emotion to break than fear.

III

Fundamentals:

III-I

Headlines:

1.) MarketWatch: Chevron CEO predicts crude will return to $100 a barrel as prices set fresh highs

2.) MarketWatch: Germany’s economy struggles with an energy shock that’s exposing long time flaws

- T5 note: The energy shock being that their energy intensive industries were far too reliant on Russian imports

3.) Bloomberg: Russia’s crude shipments hit a three month high as cuts tapered

4.) Wall Street Journal: Talks resume in Detroit as UAW threatens to widen strike

5.) Financial Times: Western policy towards Iran lacks both goals and goalposts

III-II

What You Need to Know About the UAW Strike:

Why Are UAW Members Striking?

When contract negotiations between the UAW and the ‘Big 3’ (i.e. Ford, GM, Stelantis) began to falter, the union called for a strike authorization vote in august, which was then approved by 97% of members. The union then announced that they were not interested in extending the current contract, and UAW leadership was evaluating their options if an agreement was not reached by September 14.

The UAW president has reiterated that he and his members are “fed up with the status quo” and that workers are looking for their share of the record profits their labor helps generate. Over the last four years, the three companies have increased spending on share buybacks by over 1,000%, while UAW members have seen wages rise around 6%. But this isn’t true for all the companies and is a little over exaggerated, as Ford has only bought back shares twice since 2019 in order to offset dilution from pay and debt. The UAW also argued that CEO pay has increased 40% over the same timeframe, but that just isn’t true either, as it’s only gone up roughly 21%.

What Are Workers Demanding?

The demands are a complete overhaul of the contract, both pay and conditions. The first thing on the list for the union is eliminating the tier system that allows companies to forbid some workers from joining the union. The UPS Teamsters were able to negotiate an end to their tier system over the summer, and the UAW wants to accomplish the same thing.

As for pay, members are proposing around a 40% increase over the next four years that the companies apply a cost-of-living adjustment (COLA) to, in order to support employees during times of high inflation. For retirement, the union demands that all workers receive a defined benefit pension and that medical care be reestablished for retirees.

They also want to transition to a four-day workweek, expand leave programs for families, and a stipulation that if a plant closes, that companies would be required to pay former workers to do community service. This is where they lose us a little bit. I get wanting to receive more pay and what they’re asking is more than fair, but more pay for less work with more time off allowed is a tough ask, and it’s highly unlikely a four-day workweek will be given. You would also need to think about the supply chain issues with that, and the potential mountain of extra costs it would bring onto the companies but that is for tomorrow’s report.

Offers Made by the Big 3:

So far, the Big 3 have offered wage increases of around twenty percent over the life of the contract. Ford and Stellantis have agreed to implement a COLA to ensure worker pay keeps pace with inflation. Ford has also offered five weeks of paid leave and seventeen paid holidays.

The two sides remain far apart on nearly every demand being made, and GM and Ford have announced that layoffs may begin as production is disrupted by the strike. Layoffs of non-union members are one-way companies can limit solidarity between workers but also motivate those on strike who feel even more pressure to stand up for the unprotected workers they work with.

Will More Plants Strike?

As of right now, there are three sites employing around 13,000 workers that have been called on to strike. The UAW has taken a new approach to this labor action by only selecting a few plants at a time to strike. On Monday, UAW president Shawn Fain said more plants will be called on if “serious progress” isn’t made with the companies by noon on September 22.

IV

Market Psychology & Final Thoughts:

Futures are still edging down as we head towards the open. Crude prices are continuing to rise as well as bond yields, with overseas markets (particularly Europe) are mixed so far through the bulk of their session. The markets have been flip flopping between euphoria, caution, and panic in what seems like every day. Good news is bad news, bad news is good news, mediocre news has markets on the edge of their seat, waiting for the next headline. It is truly a bizarre environment, but that’s what it is at this point in time. As always, we hope you found this useful, learned a few things, and have an absolutely splendid day.