The Take Five Report: 10/4/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: -1.37%

- Dow: -1.29%

- Nasdaq: -1.87%

- Russell 2k: -1.69%

Markets opened the day just below the breakeven mark. A rapid sell off began a few minutes following the opening bell, and stocks would continue to slide throughout the session without much relief after a wild day on Wall Street. Kevin McCarthy was ousted as speaker of the House following the close yesterday. Matt Gaetz pulled it off in an absolutely wild turn of events that was a surprise to be sure, but a welcomed one.

Asia:

- Shanghai: closed

- Hong Kong: -0.78%

- Japan: -2.28%

- India: -0.44%

Asian markets finished vastly lower in this morning’s session, with Korean and Japanese indexes pacing the region with over -2% declines following the continued jump in U.S. Treasury yields, with both countries being massive holders of them.

Europe:

- UK: -0.54%

- Germany: -1.06%

- France: -1.01%

- Italy: -1.32%

European stocks closed lower once again in yesterday’s session as market participants continued to digest poor economic data coming out of the region. All sectors and industries finished in negative territory. The debt heavy utilities sector dropped -2.7% with higher for longer at the forefront, as is the case with U.S. utility stocks as well.

I-II

U.S. Sectors Snapshot:

Communication Services: -1.40%

Consumer Discretionary: -2.59%

Consumer Staples: -0.70%

Energy: -0.02%

Financials: -1.67%

Health Care: -0.91%

Industrials: -0.74%

Info Tech: -1.82%

Materials: -0.30%

Real Estate: -1.90%

Utilities: +1.17%

II

Technicals:

II-I

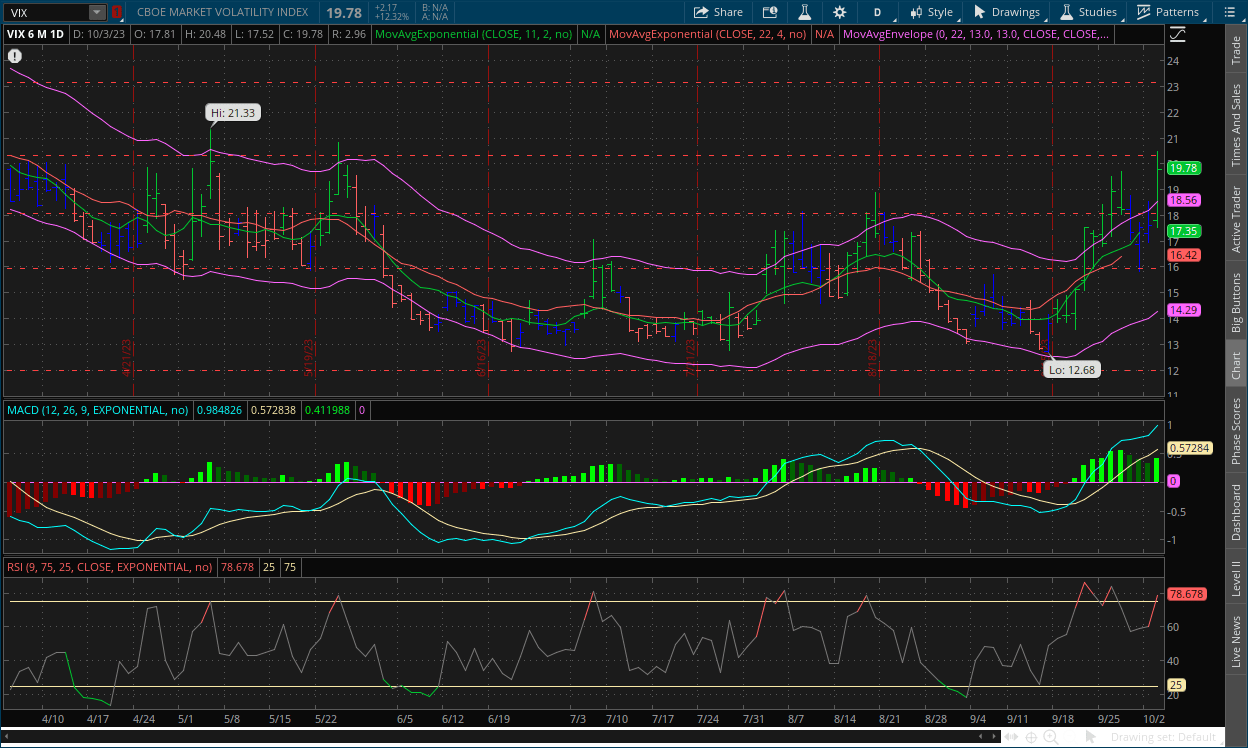

Volatility Index: (VIX)

Tuesday Recap:

The VIX opened at $17.81 and slid to a low of only $17.52 in the early premarket. Prices jumped on the day to a high of $20.48, the highest level since May 24, before ultimately closing at $19.78.

Daily Chart:

Strength moved in favor of the VIX bulls as they snapped their three day rest period while inertia accelerated even more to the upside.

Prices broke out above the $18 level again in a big way yesterday. The dip back below that mark looks to just be a false breakout. We thought we might see prices consolidate for a short time but if a breakout were to occur, then expect it to the upside, which is what we ended up seeing here but it was a little sooner than expected and the likely catalysts were Kevin McCarthy's ousting and the dysfunction going on in Washington as well as the strong JOLTS data.

II-II

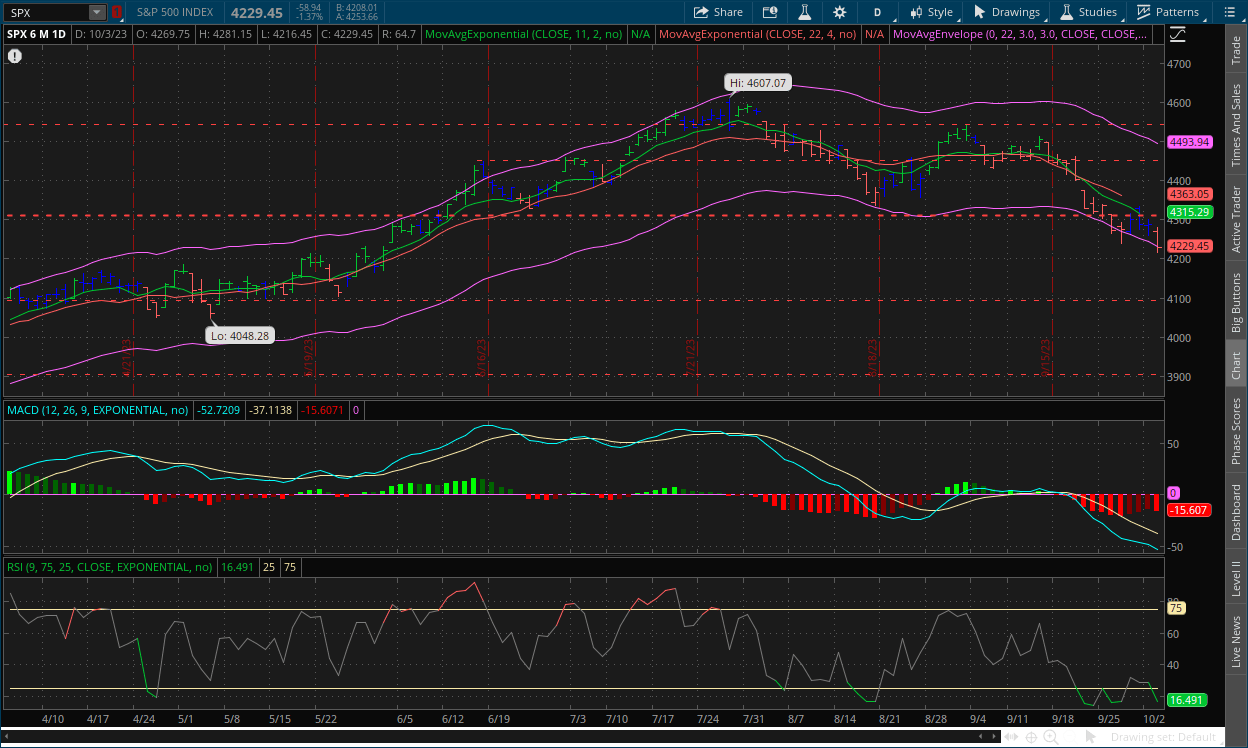

S&P 500: (SPX)

Tuesday Recap:

The S&P opened the day slightly lower at $4,269, and fought to a high of only $4,281 before sliding throughout the session. Prices found a bottom at $4,216, and ultimately closed the day at $4,229.

Daily Chart:

Strength moved in favor of the bears in yesterday’s session following the cooldown they took over the last couple of sessions while inertia accelerated more to the downside.

Bears continued to move prices strongly lower yesterday after a few sessions of consolidation. The MACD Lines are gaining more separation from each other, and are continuing to move deeper below the centerline, indicating that this trend is becoming harder for the bulls to break. The MACD-H is close to developing a bullish divergence however, and it’s something we’ll have to keep an eye on as time progresses.

III

Fundamentals:

III-I

Headlines:

1.) MarketWatch: U.S. 30 year bond yield tops 5% as Washington dysfunction rattles investors

2.) MarketWatch: Kevin McCarthy ousted as Speaker of the House

- T5 note: Well that was fast

3.) MarketWatch: Saudi Arabia says it will maintain production cuts that have helped drive oil prices up

4.) MarketWatch: Ford says that its ‘strongest proposal’ for UAW has hit the negotiation table

5.) Wall Street Journal: Bond selloff threatens hopes for economy’s soft landing

6.) Bloomberg: U.S. 30 year mortgage rate tops 7.5% for first time since 2000

7.) Financial Times: Germany seeks ‘grand bargain’ with France over energy

- T5 note: If they didn’t rely on Russia so much they wouldn’t need a grand bargain from France

III-II

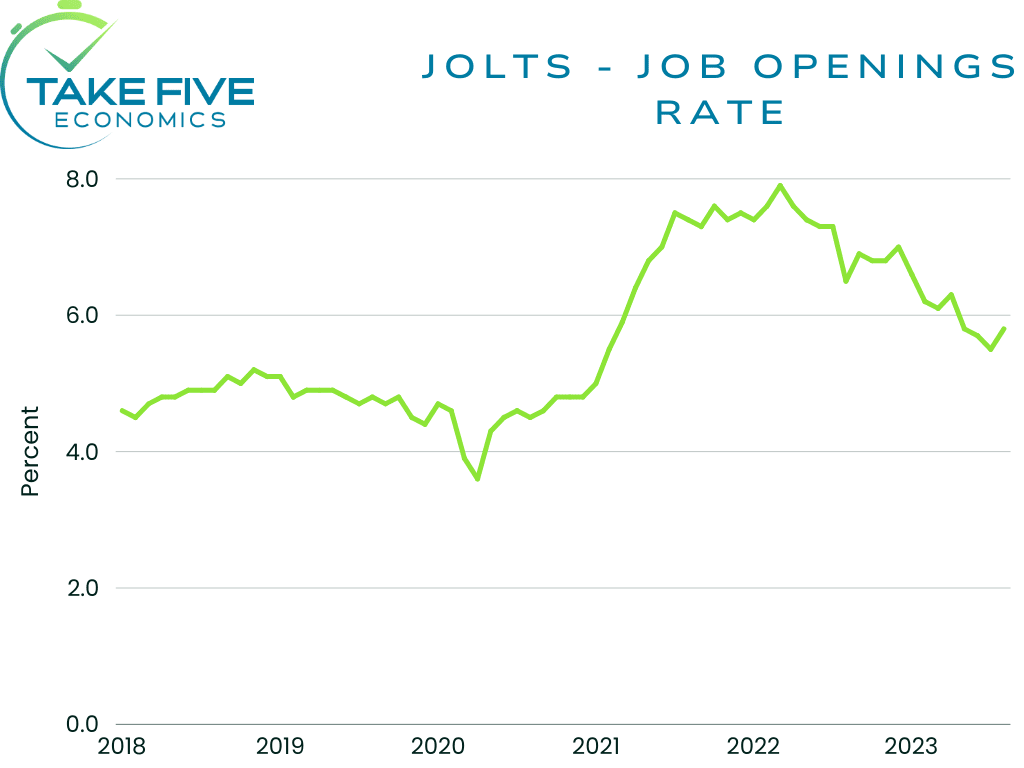

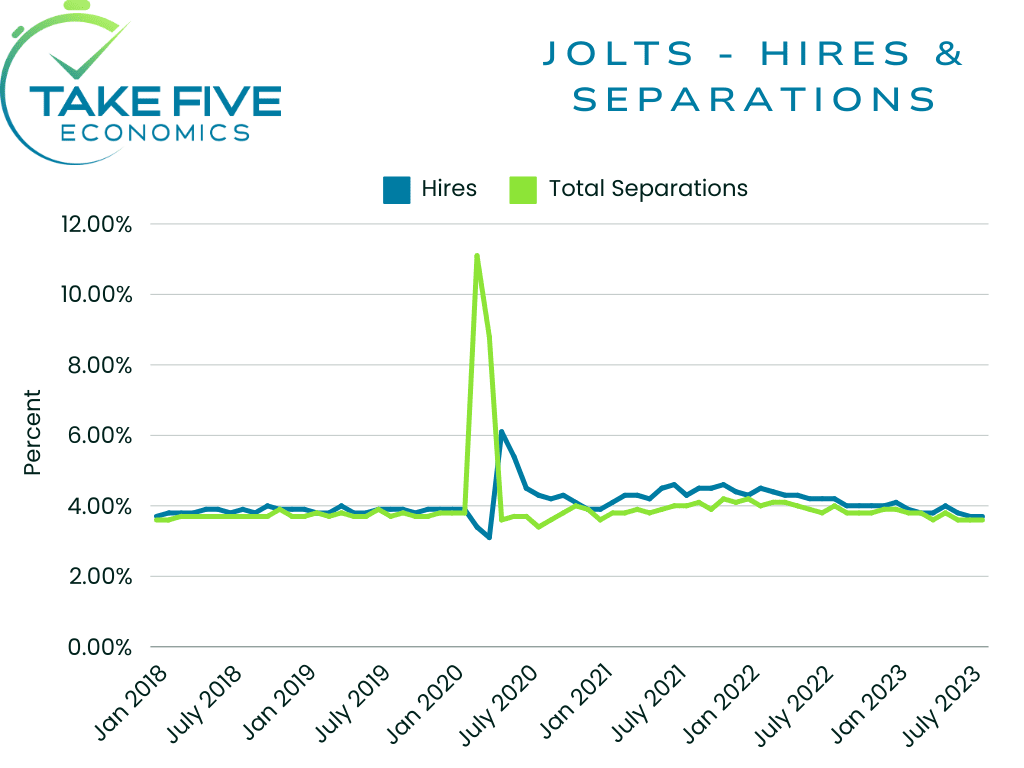

JOLTS Data for August:

Highlights:

|

Month/Index: |

Job Openings: |

Hires: |

Separations: |

|---|---|---|---|

|

July 2023: |

8.920m (r) |

5.8m |

5.5m |

|

August 2023: |

9.610m |

5.9m |

5.7m |

The number of job openings increased to 9.6 million on the last day of August. Over the course of the month, the number of hires rose to 5.9 million, while total separations increased to 5.7 million. Within separations, quits were up from 3.5 million in July to 3.6 million, and layoffs and discharges increased from 1.6 million to 1.7 million.

Finer Details:

Job Openings:

On the final day in August, the number of job openings for the month increased by 690,000, with a rate increase of 0.5% to 5.8% compared to 5.3% in July. Openings spiked in professional and business services by 509,000, carrying the bulk of the report. Notable increases were also seen in finance and insurance (96,000), state and local government education (76,000), nondurable goods manufacturing (59,000), and federal government (31,000).

Hires:

The number of hires for the month increased by 35,000, with the rate remaining unchanged at 3.7%. The number of hires changed very little in all industries, so nothing too much of note here.

Separations:

Remember: Quits are generally voluntary separations initiated by the employee. The quits rate can serve as a measure of workers’ willingness or ability to leave jobs, i.e. a measure of how strong the job market is. Layoffs and discharges are involuntary separations initiated by the employer.

Total separations in August increased by 38,000, with the rate remaining unchanged at 3.6%. Over the month, a notable increase was seen in accommodation and food services (105,000). Notable decreases include information (-41,000) and federal government (-8,000).

The number of quits changed little, and the rate also remained unchanged at 2.3%. Notable increases were seen in accommodation and food services (88,000), which took up the large majority of the index, finance and insurance (28,000), state and local government excluding education (21,000), as well as arts, entertainment, and recreation (18,000). The number of quits decreased in information by -30,000.

The number of layoffs and discharges changed little overall, and the rate also managed to hold steady at 1.1%. Layoffs and discharges decreased in state and local government excluding education (-39,000) but increased in state and local government education (27,000). ‘Other separations’ changed little in August at 357,000.

Putting It Together:

The JOLTS data for August supported the higher for longer narrative, as the report came in much hotter than expected and is one of the reasons why we saw bond yields rise rather significantly and markets continue to sell off in yesterday's session. The ratio of job openings to unemployed still declined to 1.51 (from 1.53), reflecting an increase in the labor force participation rate, which has correlated with mass migration over the past couple of months. In any case labor conditions still remain on the tight side. Hiring showed no signs of cooling, layoffs remained stable below pre-covid levels and the uptick in quits suggests that workers’ confidence in finding new job opportunities has remained high, another reason that supports the higher for longer narrative, markets don’t like that too much if you couldn’t tell.

IV

Market Psychology & Final Thoughts:

In a normal market environment, the JOLTS data that was released yesterday would've been taken as a positive. But since markets are so hyper focused on the Fed and interest rates, what would normally be a positive report got flipped on its head because it supports the narrative of higher for longer when some studies and analyses have shown that a strong labor market on paper may not affect inflation as much as people may think. As for the drop yesterday, besides the JOLTS, Kevin McCarthy getting ousted as speaker did not help the situation. As much as we think the move will be more productive and is a step in the right direction in the long run for Washington, we also see where it can be concerning for people who aren't as attuned. In either case however, markets are in panic mode.

Market futures are edging up in the early premarket with European markets beginning to edge up as well. Bond yields are pulling back slightly along with the VIX, and crude has fallen a few notches above $87 per barrel. U.S. indexes look to be headed towards a positive open. The ADP Employment change report was interesting, and it will be discussed in tomorrow’s report. As always, we hope you found this decently helpful, learned something about something, and have an exquisite Wednesday.