The Take Five Report: 10/19/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: -1.34%

- Dow: -0.98%

- Nasdaq: -1.62%

- Russell 2k: -2.11%

U.S. markets opened the day low, and the bulls didn’t put up much of a fight as the selling pressure was too strong from the bears. Prices declined through the close, with small caps selling off the most. Following the escalation in the middle east yesterday, fear in markets rose as well as missed earnings from key players like Morgan Stanley and Tesla.

Asia:

- Shanghai: -1.74%

- Hong Kong: -2.46%

- Japan: -1.91%

- India: -0.38%

Asian markets saw a broad selloff across the board with mainland China (i.e. Shanghai), South Korea, and Hong Kong all losing just about, or more than -2%. In terms of economic data releases, Japan recorded a higher than expected trade surplus (something the U.S. knows nothing about) of 62.4 billion yen, while Australia saw its unemployment rate dip to 3.6%. The Bank of Korea (which is their central bank) also held their policy rate steady at 3.5%.

Europe:

- UK: -1.14%

- Germany: -1.03%

- France: -0.91%

- Italy: -0.82%

European markets fell in yesterday’s session, with the UK’s FTSE pacing declines as fear continues to grow in global markets as global tensions between the east and the west rise.

I-II

U.S. Sectors Snapshot:

- Communication Services: -1.59%

- Consumer Discretionary: -2.33%

- Consumer Staples: +0.39%

- Energy: +0.93%

- Financials: -1.70%

- Health Care: -0.90%

- Industrials: -2.43%

- Info Tech: -1.23%

- Materials: -2.58%

- Real Estate: -2.18%

- Utilities: -0.94%

II

Technicals:

II-I

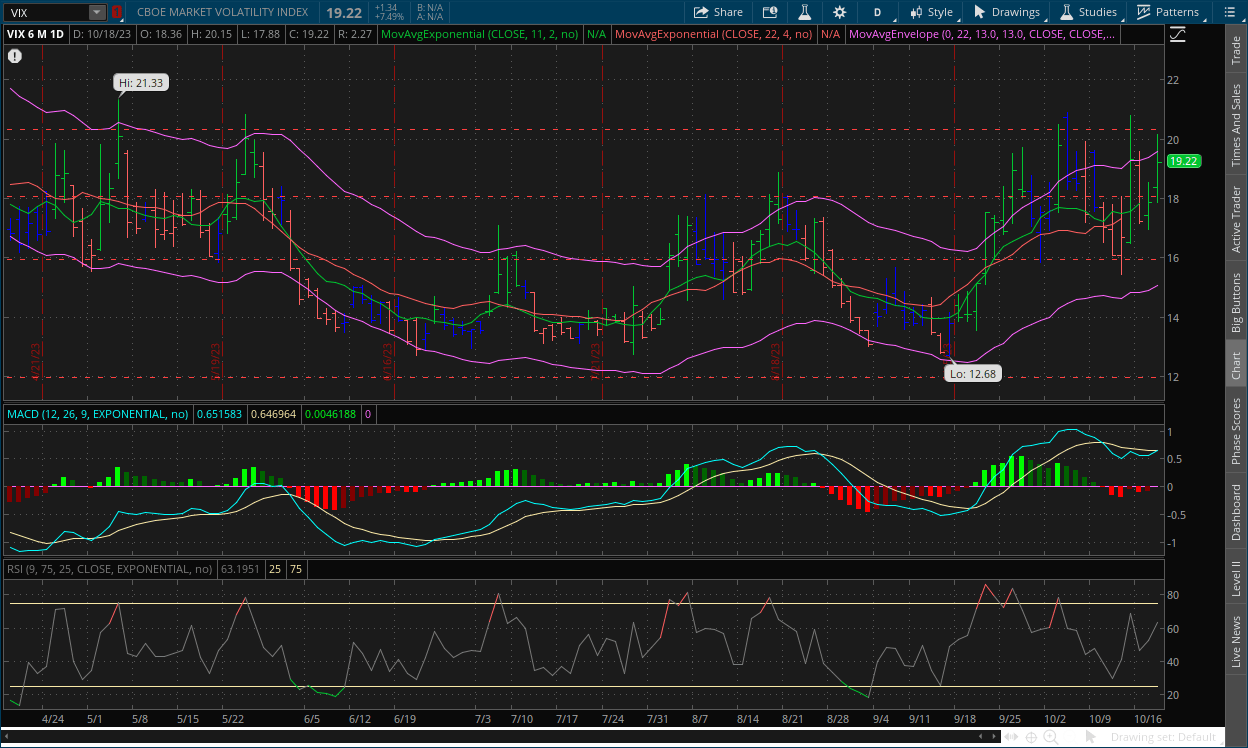

Volatility Index: (VIX)

Wednesday Recap:

The VIX opened yesterday’s session at $18.36, and worked to a low of $17.88 during premarket trading. Prices rallied throughout the day and reached the $20 resistance level again with a high of $20.15 before closing at $19.22.

Daily Chart:

Strength continued to move in favor of the VIX bulls, and they managed to narrowly push prices over the centerline as they attempt the start of a new cycle. Inertia continued to shift towards the upside, but is still in a sort of volatile flattening out/consolidation period.

Prices have hit the $20 resistance level four times now. As a general rule/principle we use in technical analysis: If prices touch, or break above a resistance level four or more times, a breakout in the same direction is more likely than a breakout in the opposite one (and vice versa). The VIX bulls really want to continue their rally, and this signal accompanied by the cross of the MACD-H (i.e. strength) shows that the bulls could be ready to make their move and begin a new cycle above the centerline. However, we don’t know if it will be as powerful as the last, but time will tell.

II-II

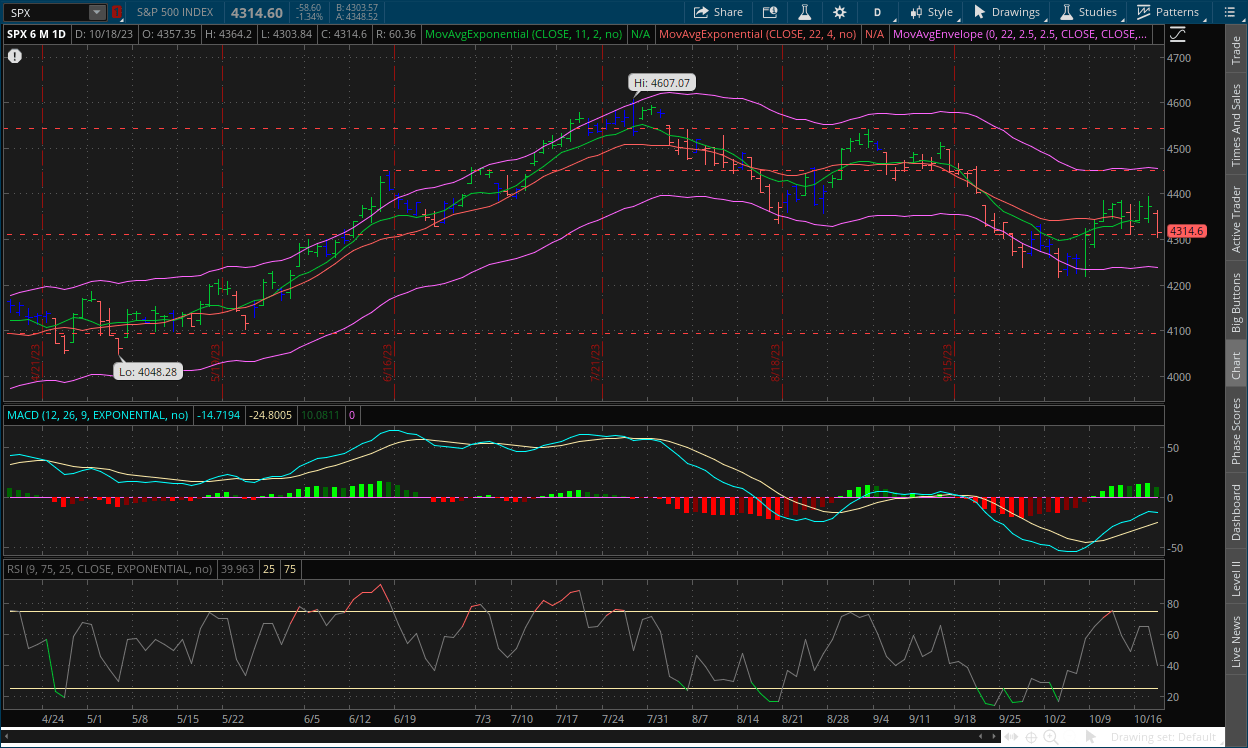

S&P 500: (SPX)

Wednesday Recap:

The S&P opened yesterday’s session at $4,357 and worked to a high of $4,364 early on. Prices declined throughout the session, and fell to a low of $4,303 before closing at $4,314.

Daily Chart:

Strength moved significantly in favor of the bears in yesterday’s session, their first significant move in the last few weeks. Inertia edged in favor of the bears but changed very little and remains in its flattening out period.

Following yesterday, the bears will likely try to make another push in retaking the $4,300 support level. Bulls failed to break the $4,400 resistance level, and struggled when approaching it. Low amounts of buy volume showed they didn’t have the numbers or the conviction most importantly. If bears manage to break below the support and hold prices below it, expect prices to fall further, where the next test will be breaking below the previous low.

III

Fundamentals:

III-I

Headlines:

1.) MarketWatch: Wall Street warns of Black Monday repeat just in time for 36th anniversary

2.) MarketWatch: Will Jerome Powell out-hawk his Fed colleagues in Thursday speech with bond yields surging?

3.) Wall Street Journal: Treasury yields edge towards 5% amid global bond selloff

4.) Bloomberg: EU proposes delaying some ESG reporting rules

5.) Financial Times: Chinese investors’ sales of US stocks and bonds hit four-year high

III-II

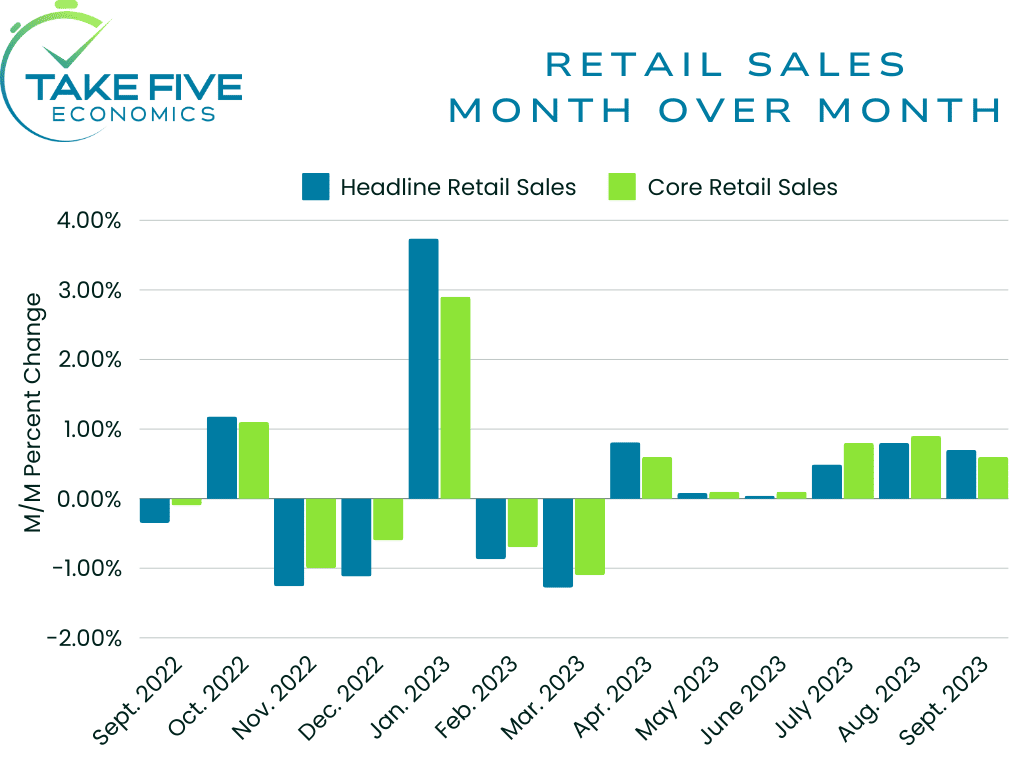

Retail Sales for September:

Highlights:

|

Index: |

August: |

September: |

Wall Street Expectations: |

Take Five Expectations: |

|---|---|---|---|---|

|

Retail Sales: |

0.8%(r) |

0.7% |

0.3% |

0.6% |

|

Core Retail Sales: |

0.9%(r) |

0.6% |

0.2% |

0.4% |

Headline:

Total retail sales increased 0.7% month over month in September, coming in much hotter than Wall Street’s expectations of 0.3% and slightly hotter than our own. The previous month was also revised upwards from 0.6% to 0.8%.

Core:

Core retail sales (retail sales ex-auto) jumped 0.6%, beating our own and Wall Street's expectations. The previous month was also revised up to a larger degree than the headline retail sales, up from 0.6% to 0.9%.

Finer Details:

Increases:

The largest increase attributable in this report was from the miscellaneous store retailer index, surging 3.0% increase in September following a -3.6% decline in August. Additional increases came from the non-store retailer index (i.e. online stores), with a 1.1% increase, motor vehicle and parts dealer index (1.0%); gasoline stations (0.9%); and food service and drinking places (0.9%).

Declines:

The largest attributable decliner in this report was from electronics and appliance stores with a -0.8% decline following a 1.2% increase in August. The only additional decliner was the building materials and garden equipment index (-0.2%). Furniture and home furnishing store sales remained flat after declining -0.6% in August.

Putting It Together:

This was definitely a much hotter report than anticipated by most on Wall Street. Most analysts expected gasoline station sales to temper after surging 6.7% in August, in which they did. But what was unexpected were the increases in the more discretionary areas, which are shown in the miscellaneous store retailer and non-store retailer indexes. This is where market participants took a pause.

In the prior retail sales report, which originally showed a 0.6% rise before the revision, market participants brushed it off due to most of the increase being attributable to the gas station index, which saw a gain of 6.7%. However, in this report, if you remove that index, retail sales still rose by 0.7%. Meaning that consumers aren’t shying away from spending on more discretionary purchases. This bodes well for Q3 GDP forecasts, but in terms of the Fed and their policy view, it isn’t ideal, and supports the higher for longer narrative once again. The rise in motor vehicle and parts sales was attributable to the UAW strikes (which are still ongoing), as consumers who were thinking of buying a new car are now buying new cars just in case they can’t in the future, or at least would have limited options, which also could have helped fuel the jump in inflation expectations in the latest consumer sentiment report.

IV

Market Psychology & Final Thoughts:

Psychology:

Market participants’ psychology hasn’t changed much since yesterday. But to reiterate, they are in reactionary mode. Given the geopolitical situation only escalates more every day, as well as our own economic data becoming more questionable, there is more downside potential than there is upside in markets at the current moment in time, but we cannot stress enough that it can flip. People tend to let go of fear much faster than they do greed, although both are very powerful emotions.

Stanley Druckenmiller came out and said that central banks, not earnings, are what move markets. We believe he’s mostly right, but it also isn't as simple as that. We believe that earnings drive the price of individual stocks in the long-term, but not the overall market. The overall market, like Druckenmiller said, is driven by central banks. The psychology of market participants when rates are low is much more euphoric than when they’re elevated, which sees them become fearful, cautious, and in reactionary mode like we’re seeing today with all eyes on Powell’s speech this morning.

When there’s low interest rates, it stimulates the consumer, allowing easier access to capital that they then use a portion of in the markets. This fuels the overall market, and some stocks that have poorer earnings or financial statements get brought along for the ride by speculators. This doesn’t make the company any better. Just take a look at any tech company’s financial statement during the Dotcom bubble and compare it to their stock price. A poor business is still a poor business, and in the end the earnings and financial statements will decide the fate of an individual company (which the central bank also does play a role in), but the central bank is the decider in the overall market direction.

Final Thoughts:

Market futures are flat as we head towards the open. Crude futures are pulling back following yesterday’s rally. Bond yields are on the rise once again, with the 10-year up 6 basis points and the 30-year up 5 basis points. European markets are falling in similar fashion to the way Asian markets did however, making today’s outlook somewhat murky for U.S. markets. The reason for the flat premarket may be because of Powell’s speech, which will likely be the key determinant for today and possibly tomorrow’s price action. As always, we hope you found this helpful, learned something about how the markets operate, and have a thrashing and dashing Thursday.