The Take Five Report: 10/24/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: -0.17%

- Dow: -0.58%

- Nasdaq: +0.27%

- Russell 2k: -0.89%

U.S. markets opened the day in negative territory following an influx of overnight volume. Stocks would bounce soon after, rallying through the first half of the day. Prices would flatten during lunch time, and would begin to reverse back to the downside and would continue that trend through the close. The Nasdaq was the only one of the major index to notch gains on the day, as tech stocks rallied.

Asia:

- Shanghai: +0.78%

- Hong Kong: -1.05%

- Japan: +0.20%

- India: closed

Most Asian markets rebounded this morning and reversed from the session’s earlier losses. Japan released the purchasing managers index for October which saw its first contraction since December of 2022. South Korean PPI climbed to 1.3% year over year compared to 1% in the prior.

Europe:

- UK: -0.37%

- Germany: +0.02%

- France: +0.50%

- Italy: +0.74%

European markets recovered from earlier losses, and would close the week’s opening session mixed as global economic and geopolitical concerns continue to weigh on sentiment. Investors are also looking ahead to the European Central Bank's monetary policy announcement this week. ECB policymakers are likely to hold interest rates unchanged when they gather in Athens on Thursday.

I-II

U.S. Sectors Snapshot:

- Communication Services: +0.72%

- Consumer Discretionary: +0.21%

- Consumer Staples: -0.27%

- Energy: -1.62%

- Financials: -0.71%

- Health Care: -0.63%

- Industrials: -0.47%

- Info Tech: +0.42%

- Materials: -1.07%

- Real Estate: -0.84%

- Utilities: -0.82%

II

Technicals:

II-I

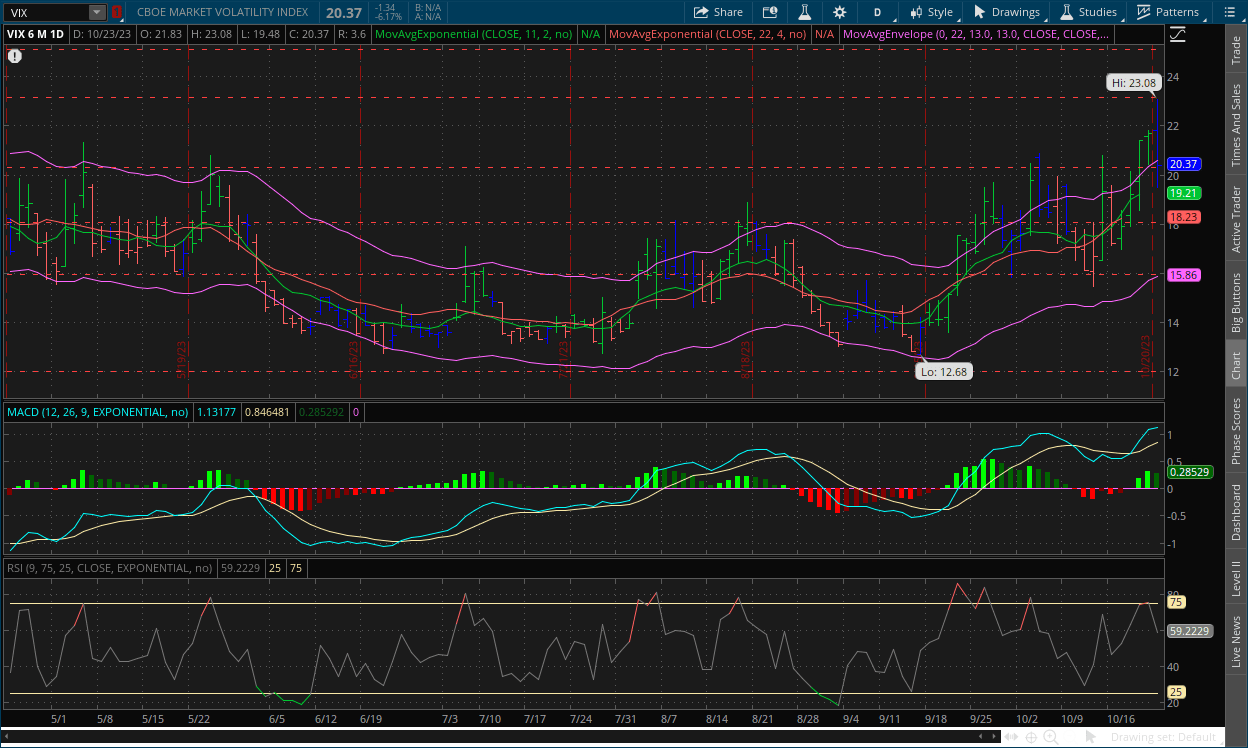

Volatility Index: (VIX)

Monday Recap:

The VIX opened Monday’s session at $21.83, just above Friday’s close and worked to a high of $23.08 during premarket hours, the highest mark since March 27. Prices soon slid throughout the day, reaching a low of $19.48 before an end of day rally brought prices to close at $20.37.

Daily Chart:

Strength moved back in favor of the VIX bears following the meteoric jump over the previous two sessions. Inertia continued to shift in favor of the VIX bulls but the slope tempered slightly.

The VIX bulls managed to keep prices above $20, but only slightly. We’re likely to see prices pull back below this level, and this looks to be a last-ditch effort by them to move prices above the $20 resistance level, which would make it a likely false breakout. Prices will most likely return to the $16-$20 consolidation range. But the key test will be seeing how the VIX bulls hold up in the next few sessions. The MACD-H also has officially traced a bearish divergence, and the move back towards the centerline is the trigger that started the signal's activation process. This means that the next move is likely downward and given the positioning and signals on the weekly chart, we're likely headed for lower volatility.

II-II

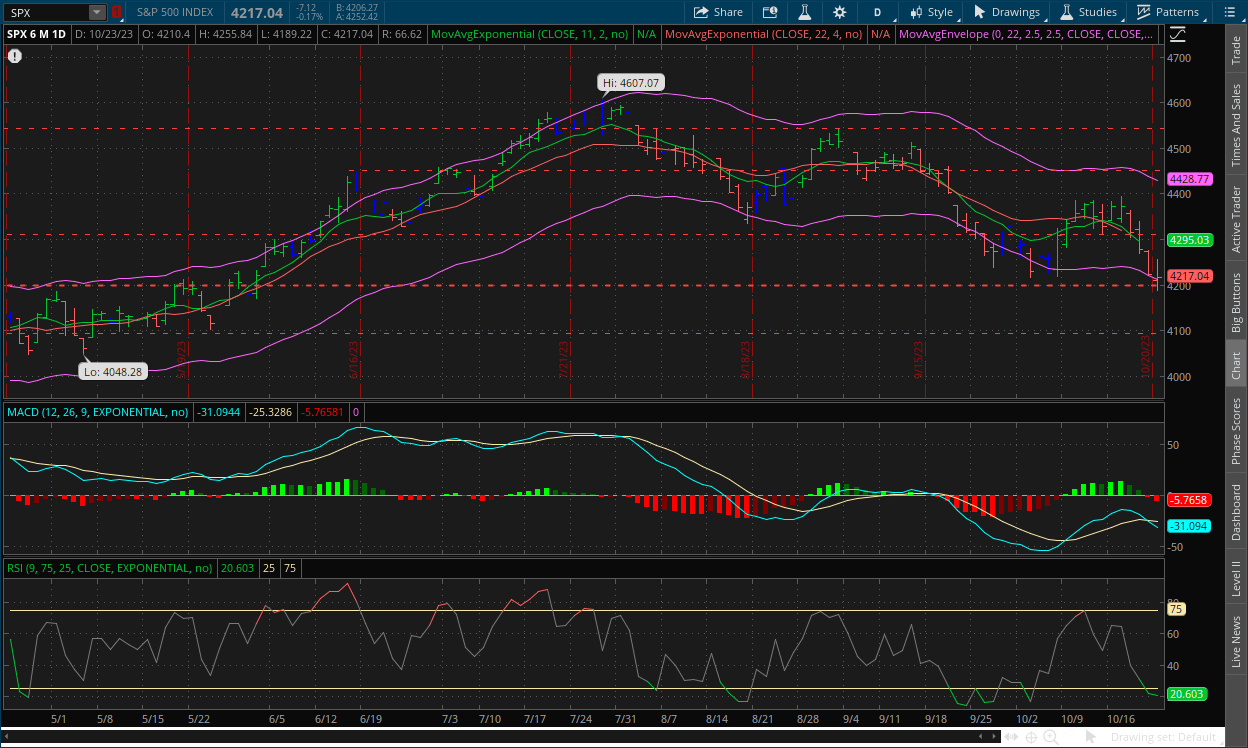

S&P 500: (SPX)

Monday Recap:

The S&P opened the session at $4,210, and reached a low of $4,189. Prices rallied to a high of $4,255 before closing at $4,217.

Daily Chart:

Strength moved in favor of the bears in yesterday’s session, as they fully broke below the centerline with authority. Inertia continued to shift towards the downside and is adding more downward pressure to stocks.

The bulls held prices from breaking below the $4,200 with conviction, as this point looks to be stronger than the bears may have anticipated. The bulls are starting to gain more of an edge in the technical signals now, and another bullish divergence may be developing in the MACD-H, which would make it a triple, and it indicates an underlying weakness in the bears. The S&P could be ready to rally sooner rather than later.

III

Fundamentals:

III-I

Headlines:

1.) MarketWatch: Coca-Cola stock jumps after profit and revenue beat expectations as price and volume rise

- T5 Note: Coke is king. It’s called a durable competitive advantage

2.) MarketWatch: General Motors posts better than expected earnings and defends latest offer to UAW

3.) Wall Street Journal: China strips missing defense minister of government posts

T5 note: We all know what happened here

4.) Bloomberg: A major driver if U.S. equities in the past decade is fading fast

T5 Note: Share buybacks

5.) Financial Times: Eurozone economy’s outlook worsens, shows business survey

III-II

Per Barron's - Tech Stocks Are More Appealing as Earning Season Starts Up:

Highlights:

While tech stocks of major companies have gotten hammered recently, forecasts for their earnings have risen, so the group is looking increasingly attractive from Big Tech all the way down. The Technology Select Sector SPDR ETF (ticker: XLK) is down just over -9% from its record high, hit in late July, mainly because long-dated bond yields have taken off. Higher yields make future profits less valuable in current terms, which means investors aren’t willing to pay as much for the earnings fast-growing tech companies are expected to pump out years from now. As a result, valuations of tech companies have fallen.

However, higher than expected earnings for technology companies such as Netflix (NFLX) have been the most recent source of optimism. All of the five tech companies in the S&P 500 that had Q3 readings through Friday turned in higher profits than Wall Street expectations. Total sales for those five were about in line with estimates, while earnings per share (EPS) were about 6% higher. This is a positive combination. If profits are well ahead of forecasts while sales are just a little bit better than expected, it means profit margins are coming in better than anticipated.

Breakdown:

Quick Tangent:

We just want to get out of the way that the last little sentence in this Barron’s piece isn’t always the case. Here they’re talking about EBITDA, which is Earnings Before Interest, Taxes, Depreciation and Amortization. In other words, additional and very real expenses. Wall Street analysts like to forget about these expenses and focus mostly on gross profit and gross profit margins, which is EBITDA. But we prefer net profit and net profit margins which is earnings after all expenses. The point we're trying to make is that yes, this logic would increase their gross profit margins, but there could be additional debt that increases interest (and today’s environment, higher rates), additional property purchases that add to depreciation charges, or whatever the case may be that could decrease overall margins and something that may put a hole in their financial statements if it is overlooked. Anyways, back to the task at hand.

Tech Growth Combined with High Interest:

Higher yields have put much more pressure on tech companies, at least in terms of mid and small cap ones in today’s environment. As a refresher: large cap companies have played this market perfectly. Large cap tech companies are able to borrow money (i.e. issue bonds) at 4% interest but can deposit their cash in a money market fund for 5%-6% interest. For example, if they have $1 billion in cash, and want to borrow $1 billion, they’ll issue $1 billion worth of long-term bonds and owe 4% interest on that principal amount. But they still have that $1 billion in cash, so they will then deposit that in a money market fund and earn say 5.5% (happy medium) with full liquidity. Meaning that they’re earning 1.5% on borrowed money, essentially becoming a bank themselves. The reason they’re able to do this is because of how favorable their corporate credit ratings are with banks. Small and mid-cap companies don’t have this luxury, and higher yields and interest rates are what is squeezing them right now because they can’t borrow at the same interest large caps can.

For the tech sector as a whole, the reason why higher yields put pressure on them is because their growth is fueled by debt, which was fantastic in the easy money days of the 2010’s and the two years after covid. But now, they can’t grow to that extent anymore unless they are large caps because of higher interest rates, i.e. the cost of borrowing is much higher, and this has indeed hurt tech valuations.

Strategy:

But the strategy that Barron’s is trying to get across here is a valid one in terms of speculation. If you focus on what Wall Street preaches with EBITDA and the potential favorable earnings catalysts, it may be a safe bet to look for swing trades in the long direction. You’d likely be getting these companies at their short-term discount rate, and if they’re earnings prove better than expected (which seems like the likely case), you’ll likely be looking at an exceptional take. And for those plays that don’t work out the way you thought they would, keep your stop losses fairly tight and have a strong sense of risk management. Use the positive fundamental catalysts in your technical trades, and if both are giving signals in the same direction, the psychology towards that stock will likely be in the favor of your position.

IV

Market Psychology & Final Thoughts:

Psychology:

The bulls are putting up a fight against the bears as they approach, or have broken through key levels in prices. The last few days have been positive for earnings, giving the bulls some momentum. Positive catalysts are across the board this week with big tech earnings and the GDP report. As of today, the bulls have an edge over the bears in terms of technicals, and the fundamentals could be shifting in that direction depending on how everything turns out.

Final Thoughts:

U.S. markets opened the day deep into positive territory, with European markets starting to rally back from earlier losses as well. Crude is continuing to fall as well as yields, making today’s outlook fairly rosy. Today the U.S. has the S&P services and manufacturing PMI being released, so not much in terms of economic data but some key earnings have already been reported with positive results and more are on tap for after hours and later in the week. We hope you found this helpful, learned something about the kind of shady shit large caps do (but hey the more power to them), and have a terrific Tuesday.