The Take Five Report: 10/26/23

I

Markets:

I-I

Global Market Recap:

United States:

- S&P: -1.43%

- Dow: -0.32%

- Nasdaq: -2.43%

- Russell 2k: -1.67%

The S&P and Nasdaq would open the day down, while the Dow opened on a positive note. The S&P and Nasdaq slid through the close, but the Dow was resilient and managed to stay within a tight trading range throughout the day and outperformed the other indexes.

Asia:

- Shanghai: +0.48%

- Hong Kong: -0.24%

- Japan: -2.14%

- India: -1.41%

Asian markets saw a broad selloff in this morning’s session, with Australia’s indexes closing at a one year low while mainland China managed to buck the region's broader trend. South Korea’s GDP grew at 0.6% in Q3, slightly beating expectations.

Europe:

- UK: +0.33%

- Germany: +0.08%

- France: +0.31%

- Italy: -0.52%

Major European markets closed slightly higher in yesterday’s session with participants largely digesting quarterly earnings, the outlook on interest rates and geopolitical tensions. Turkey’s market plunged more than -7% amid concerns of a souring relationship with Israel and the nation’s central bank decision.

I-II

U.S. Sectors Snapshot:

- Communication Services: -4.09%

- Consumer Discretionary: -1.69%

- Consumer Staples: +0.62%

- Energy: -0.07%

- Financials: -0.09%

- Health Care: -0.90%

- Industrials: -1.27%

- Info Tech: -0.87%

- Materials: -0.96%

- Real Estate: -2.10%

- Utilities: +0.78%

II

Technicals:

II-I

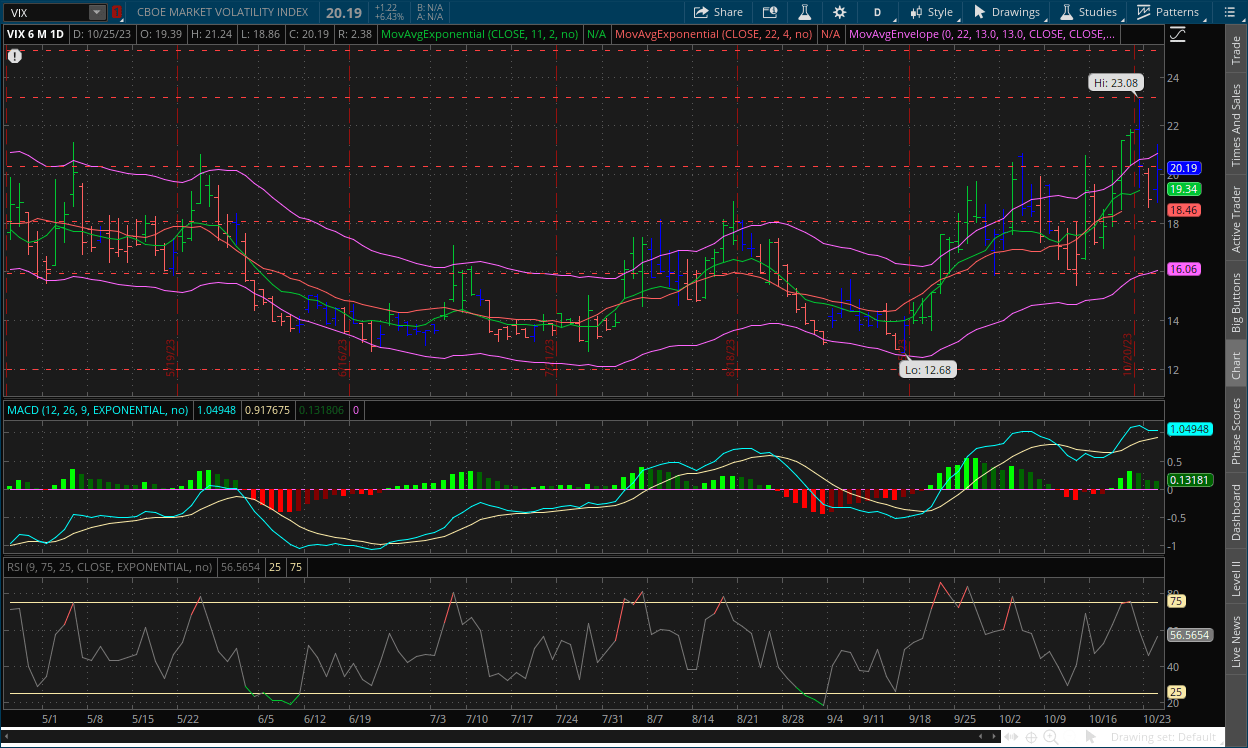

Volatility Index: (VIX)

Wednesday Recap:

The VIX opened Wednesday’s session at $19.39, rebounding from Tuesday’s close. Prices dropped to a low of $18.86 during premarket hours, and would rally throughout the day to reach a high of $21.24 before closing at $20.19.

Daily Chart:

Strength continued to edge in favor of the VIX bears despite the bounce on the day for the third straight session, although their momentum back downwards is tempering. Inertia remained moving towards the upside, but the slope isn’t as steep as it was a few days ago.

A bearish divergence has been created in the daily MACD-H (i.e. strength), as the newest price peak is higher than the previous, while the MACD-H’s corresponding peaks are the opposite. This signals weakness in the current trend from the VIX bulls, and that a reversal may be coming sooner rather than later especially since the divergence is in its activation period. This also is accompanied by a breakout above an extremely strong resistance point at $20, making the signal even more favorable.

II-II

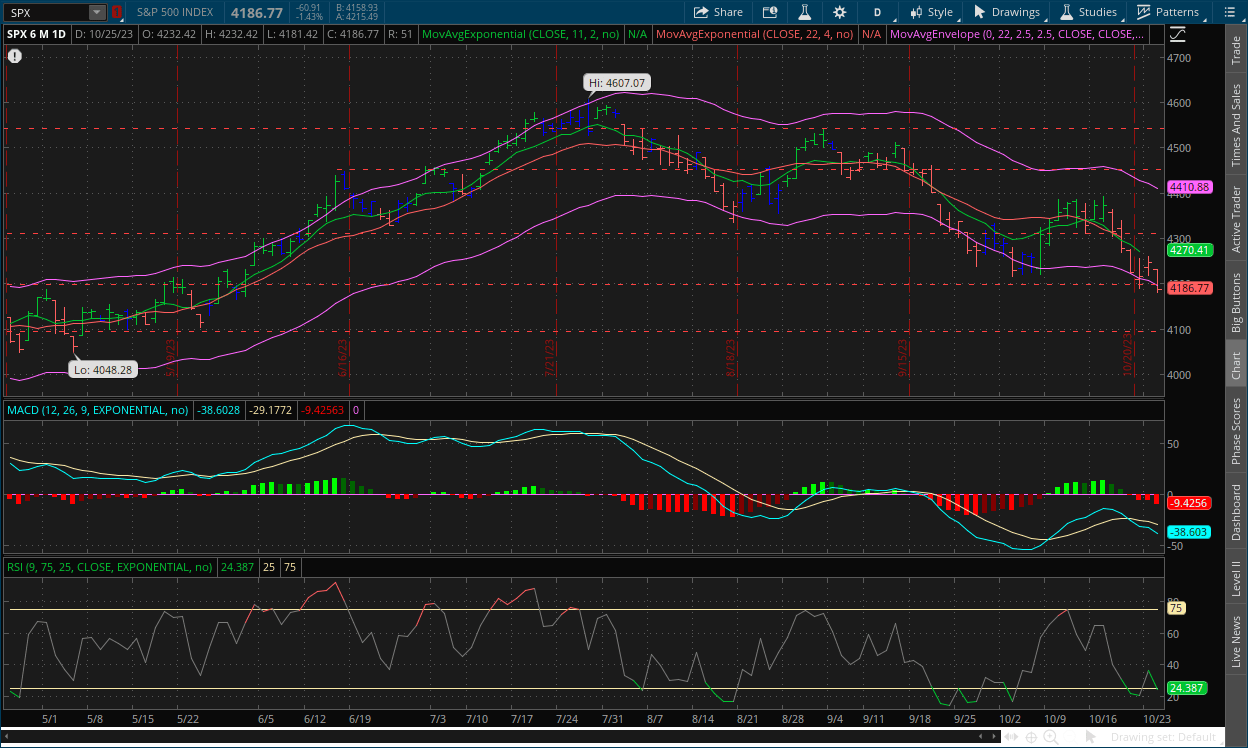

S&P 500: (SPX)

Wednesday Recap:

The S&P opened yesterday’s session at $4,232, which also turned out to be the high for the day as this one was all bears. Prices declined throughout the day, and found a low of $4,181 before closing at $4,186.

Daily Chart:

Strength continued to move in favor of the bears as they moved deeper below the centerline. However, this is a textbook setup for the formation of a bullish divergence, and is something we will continue to keep our eyes on in the days ahead. Inertia continued to edge downward, as it hasn’t shown any signs of slowing down quite yet.

The bullish divergence hasn’t quite fully developed yet as the bearish divergence has in the VIX, but it’s on its way, and given the signal appearing in the VIX, the S&P has a higher chance of developing it as well but it's not a guarantee. Like the VIX, the possible signal is also developing at a key support level (i.e. $4,200) with a breakout below it, again making the signal even more favorable towards a reversal if it were to occur.

III

Fundamentals:

III-I

Headlines:

1.) MarketWatch: GDP shows U.S. economy expanding 4.9% in third quarter

- T5 note: This will be covered tomorrow

2.) MarketWatch: U.S. new home sales just defied gravity, surging to highest level since February 2022

3.) MarketWatch: U.S. Trade deficit in goods widens 1.3%, neutral for GDP growth in third quarter

4.) Wall Street Journal: Ford reaches tentative labor deal with UAW six weeks into historic strike

5.) Wall Street Journal: Euro, bond yields edge down after ECB keeps interest rates unchanged

6.) Bloomberg: UPS cuts forecast after profit misses estimates on higher costs

III-II

U.S. Oil Giants Returning Home:

Exxon Mobil & Chevron Acquisitions:

As the world becomes more and more fractured, the two largest crude oil producers in the west are starting to focus their investments closer to home. As we discussed briefly on Tuesday, Chevron said that it was acquiring Hess in a $53 billion deal that gives it access to one of this century’s biggest oil finds in the South American country of Guyana, as well as allows them to double down on shale production by expanding its presence to North Dakota. Both regions are established oil producers with (obviously) limited geopolitical tensions, and offer Chevron new assets with limited risk. The deal follows the megadeal in the U.S. shale patch (Permian Basin; located in Texas and New Mexico) by Exxon Mobil, which acquired Pioneer Natural Resources in a $60 billion merger that anchors its future to the region.

These two acquisitions in quick succession are signaling that Chevron and Exxon Mobil, the two largest producers in the west, are increasingly turning their attention closer to home as international investments are becoming more complicated by the threat of expanding regional conflicts in Ukraine and Middle East.

Diversification:

Exxon Mobil and Chevron have built their businesses for decades through expansion across the globe, looking for exploration opportunities as investors have pressured the companies to add to their booked reserves, a key metric used by shareholders to value producers. As a result, oil giants operated in higher risk areas. But the emergence of U.S. shale has eased pressures as companies are now able to drill more on the domestic front, where there’s low risk of war or sudden regime changes.

In a call with analysts earlier this month, Exxon CEO Darren Woods said that diversification allowed the company to manage geopolitical risks, but that Exxon also had to make sure that it had access to low-cost production, including in the U.S. For Chevron, by acquiring Hess, it continues to diversify their own portfolio by getting additional shale assets, a more solid infrastructure, and access to Guyana along with Exxon, which Chevron has called an extraordinary asset. Guyana’s proximity to the U.S. and relatively stable politics are similarly appealing to the oil companies. The country has exhibited respect for contracts for oil concessions there, allowing Exxon and Chevron to tout their investments as low-risk projects that will deliver new oil barrels to the U.S., potentially lowering gasoline prices, and gives a major foothold in regions that are also of strategic importance to the U.S.

Chevron’s announcement was made two weeks after Israel ordered the company to shut down natural-gas production at one of its two major offshore platforms in the Eastern Mediterranean Sea as the war between Israel and Hamas escalated. The order was a reminder of the risks oil giants face in a region marred by violence that has previously jeopardized ambitious energy projects. The companies also face investors’ demands that they focus on returns and steer away from the potentially profitable but costly and risky frontier exploration of untested regions that vaulted them to their global status.

Exxon has planned since 2018 to sell at least $15 billion worth of assets as it shrinks its global footprint and focuses on its more valuable assets. It has sold out of projects in Chad and Cameroon, completely pulled out of Russia, and made progress on its goal to shed additional holdings in Iraq and Nigeria. Meanwhile, Chevron since 2019 has unloaded assets in Azerbaijan, Denmark, the U.K. and Brazil, among others.

Following the Pioneer deal, about 45% of Exxon’s production will come from the U.S., up from roughly 31% before it, according to JPMorgan Chase. Both Exxon and Chevron said their recent shale acquisitions would strengthen U.S. energy security, reflecting concerns that oil supplies may become harder to come by as war rages in Ukraine and diplomats rush to the Middle East to try to prevent a regional conflagration involving Israel and Iran-backed forces.

The companies have said that by applying skills learned in challenging regions, they will be able to recover even more oil. Exxon said it now expected to produce about 2 million barrels per day in the Permian by 2027. The focus for these companies now is investing huge amounts of dollars into low-risk assets, an aggressive approach in an effort to achieve a more conservative and diversified portfolio of assets.

U.S. Oil Ramps Up Production:

In the U.S., oil production has climbed to 13.2 million barrels a day, according to the Energy Information Administration. That’s the highest based on data going back to 1983. Data from Baker Hughes has also shown two consecutive weekly increases in the number of active U.S. rigs drilling for oil, totaling 502 as of October 20. This, along with oil giants shedding riskier assets and investing more domestically is a good sign, and something that we personally been wanting to see happen for a long time. The reasoning behind the move is bad news, but the fact that it is happening regardless is still a good thing.

IV

Market Psychology & Final Thoughts:

Psychology:

The psychology looks to be shifting underneath the surface, as is seen in the technicals with the emergence of divergences in the current trend’s strength indicator the MACD-H, and as we've said, there were potential bullish fundamental catalysts this week. With the Psychology beginning to shift, seeing it reflected in the technicals and bullish catalysts lining up, we could be looking at a reversal.

Final Thoughts:

Markets are retreating following the massive growth shown in the Q3 GDP report. Markets seem to be taking this as a bad thing, as most of the growth came through consumer spending which supports the higher for longer narrative in most people’s eyes. But they need to understand that this isn’t always inflationary, as was the case for the last 40 years, especially during the 2010’s. People have forgotten how this all works. Tomorrow’s report will consist of a full analysis of today’s GDP. We hope you found this helpful, learned a thing or two, and have a great day.